Sustainability & CSR

Round 3.2: Two steps forward, one step back

While the first draft of rules for Round 3.2 of Taiwan’s offshore wind auction brings much anticipated flexibility there is still a lot of room for improvement. Localisation items have been reduced but will factor even stronger in the awards for 2028 and 2029 – that can be up to 900MW for a single project.

By Raoul Kubitschek, Jason Wang and James McCatherin

Round 3.2 draft rules

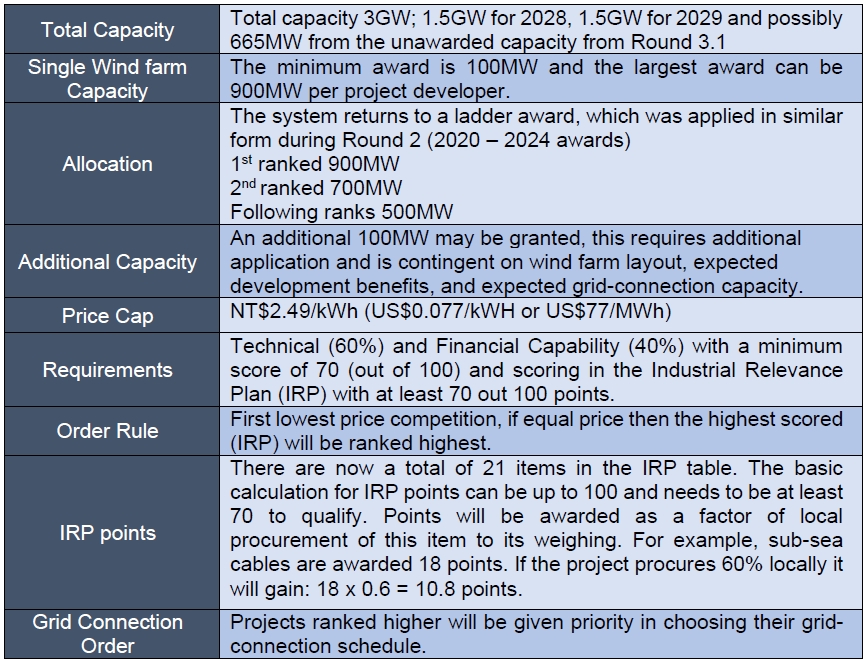

The rules for the upcoming Round 3.2 were released on 27 September 2023, with ongoing consultations with stakeholders and a final version for the guidelines and Industrial Relevance Plan (IRP) expected to be published by the end of October 2023 with a tentative prospect that the selection process will begin immediately or starting during the first quarter of 2024. The auction will award 3GW with the possible addition of the capacity not bid on during the Round 3.1 auction that awarded only 2.3GW out of 3GW available for 2026 and 2027. Overall, the current rules are broadly similar to the predictions made in our article from 12 September 2023: “Taiwan offshore wind after Round 3.1”.

The main features of the new proposed rules are:

The full set of presentations, regulation drafts can be found in Chinese on the website of the Energy Administration (EA, former BOE), under the Ministry of Economic Affairs.

Round 3.2 highlights

Pricing

The government did not change the cap of NT$2.49 per kWh (ca. US$0.077), already a move highly criticized in Round 3.1 and far from any global and local energy market developments. As of end of August 2023, the cost for Taipower, the state-owned utility, to produce one kWh was NT$4.0260 (ca. US$0.12) and Taipower loses NT$1.0045 (ca. US$0.031) on every kWh sold, as the average end-user price is only NT$3.0215 (ca. US$0.094). In the first eight months of this year Taipower has raked up a loss of NT$147 billion (ca. US$4.55 billion). The cap has only one intention: to force so called zero-bids, in which only the IRPs will be left as a weighting. It also sends the subtle message that Taipower is either not interested, or too financially troubled, to directly pursue large scale renewable energy projects.

Industrial Relevance Plan

There is a large shift in the IRP scoring and items. The Industrial Development Administration (IDA, former IDB) has largely acquiesced to demands from the industry and removed some mandatory and all voluntary items around, for example, offshore substations, vessels, operations and maintenance, environmental and other monitoring works as well as offshore works. This is partly a reaction to either the lack of established local supply chains and likely also a reflection on the outcome of Round 3.1, where a lot of voluntary items were not used. But it also came as a surprise to some local players that their market protection was removed.

The list now concentrates on 21 items with most scoring granted to underwater foundations at 18 points, nacelles (18 points), blades (18 points), and sub-sea cables (from 5 in Round 3.1 to 14 points). The way the grading system was chosen points to the fact that the IDA believes that some of the existing players still need to be protected from global competition, and on a few items, let new companies enter the market or extend some of the services of existing local players. The IDA can already count its first big success with the joint venture between Walsin Lihwa and NKT, a Danish market leader in the cable segment. Both companies already signed a multi-billion NT dollar deal in February this year with the aim of producing cables by 2027. Only two days after the EA hearing, they held their groundbreaking ceremony in Kaohsiung City.

Capacity Increase

The EA made a major concession to industry demands by introducing larger capacity awards. Basically, capacity of the first ranked projects could potentially be up to 1GW (900MW + 100MW) while second projects could be up to 700MW and the third and any further ranked projects up to 500MW. With at least 3GW up for auction, a minimum of five developers could win awards. If the auction were to use unsold capacity from Round 3.1, up to six developers could walk away with projects. There are now at least seven developers who either already have conditional Environmental Impact Assessments (EIA, a minimum requirement) in hand or could achieve this within the next five to six months before the auction would close, at the earliest. Due to overlaps in proposed offshore wind project areas (in which multiple parties can compete and only one can win) and the timing needed to obtain EIAs, it remains to be seen if there will be sufficient competition for the full available capacity to enter the auction.

It’s all about the Industrial Relevance Plan

The Ministry of Economic Affairs has been very successful in the past in designing their auction processes to push through its own objectives, and this time is no different. The current proposed regulations are aimed at increasing localisation – while there are now fewer items, due to the staggering of the award, most developers will gear up to secure as many points as possible – unless they want to settle for a 500MW award. There are only a few local companies active in the highest scoring item categories – in some cases no more than three and often only one. In this way, the IDA has made sure that not only will existing companies receive orders but those that are either new or have a need for a comeback will have the necessary orders and, with them, likely take advantage of the opportunity to extract higher prices for their offerings.

The Achilles heel of designing the auction this way, is higher energy prices for the CPPA off takers, who will ultimately pay for the IDAs industry policy, which has the potential to create an adverse effect for the offshore wind energy industry. There is a strong likelihood of further local supply chain bottlenecks. Unfortunately, the market lacks a variety of domestic suppliers, which not only could lead to a lack of competition but also insufficient supply to meet demand. Thus, it is likely that the new scoring system may create more supply chain bottlenecks and cost increases, as demand far outstrips supply.

Another weak point is that experienced developers with greater financial and technical capabilities may have no incentive to compete. There are only a few developers financially and technically capable of building larger offshore wind farms globally, but also demonstrated in the ongoing Round 2. Given their experience and understanding of risk they may decide to pull out again or only go for 500MW awards, which have lower IRP scoring requirements. This will also have the effect that lesser experienced developers might overplay their cards by signing off on too many localisation items in a feverish effort to try to secure 900MW projects, which could ultimately lead to either abandoned projects or massive delays and cost overruns in the construction of these wind farms.

Effective in designing auctions, but not in delivery

The government has had a certain degree of success in auction design and awards, but so far it has had no success in making sure that projects will be delivered on time. The 2026 and 2027 targets for Round 3.1 are highly unlikely to be met. This is an opportunity to design Round 3.2 to place more emphasis on the ability to deliver – and for this there needs to be a reconsideration of the IRP weighing, the price cap, as well as the selection criteria, for example weighing a successful track record and financial health higher than the IRP Plan.

Raoul Kubitschek has worked in Taiwan’s renewable energy sector since 2008 and is currently the Taiwan Country Manager for NIRAS. He is concurrently Co-Chair of the ECCT’s Energy and Environment committee.

Jason Wang is a Senior Economist for NIRAS, a Danish multi-disciplinary engineering company, focused on energy policy and market forecast consultancy for clients and supporting NIRAS’ efforts in Environmental Social and Governance (ESG) offerings in the APAC region.

James McCatherin is a Consultant working for NIRAS. He supports social & political considerations for Offshore Wind as well as Environmental Social and Governance (ESG) in Taiwan and the APAC region. His background is in International Development and Political Science.