Sustainability & CSR

Taiwan offshore wind after Round 3.1

Results from the latest auction were disappointing and interim renewable energy targets will not be met but sensible policy adjustments could revive momentum.

By Jason Wang, Raoul Kubitschek and James McCatherin

Despite awarded capacity in Round 3.1 auctions falling short by 665MW, Taiwan at least managed to secure more projects than anticipated and continues moving forward in the pursuit of its energy goals. Current market conditions and sentiment have led to an element of pessimism and uncertainty in the industry, but Taiwan has the opportunity to remain an important offshore wind market in the region, if it manages to adjust its upcoming Round 3.2 rules.

Round 3.1 awards

With a total of five project developers completing the final signing procedures, Taiwan's offshore wind (OSW) Round 3.1 concluded on 30 August 2023. This ‘successful’ auction may be seen as a relief to an industry, that is struggling against literal and figurative headwinds not only in Taiwan but also globally. Despite the original available capacity of 3GW for the auction, the awarded capacity from Round 3.1, scheduled for 2026/27 grid connection falls short, standing at only 2.335GW.

Awarded capacity for Round 3.1

| Wind Farm | Developer | Capacity (MW) | Commission Year |

| Feng Miao | CIP | 500 | 2027 |

| Formosa 3 -(Haiding 2) | CORIO / TotalEnergies | 600 | 2026 |

| Hai Xia Phase 2 | Skyborn | 300 | 2026 |

| Formosa 4 | SRE | 495 | 2027 |

| Ocean (Huan-Yang) | EDFR / Taiya | 440 | 2027 |

| Total | 2,335 | - | |

Round 3 has been off to a very slow start overall. Continued delays have added to market uncertainty, affecting the decisions of project owners, investors, and supply chain alike. Based on the original Bureau of Energy (BOE) timeline for Round 3, that will aim to award 15GW between 2026 and 2035, Round 3.1 administrative contracts were scheduled to be settled in 1Q23, with auctions for Round 3.2 of 3GW for 2028/29, to be held in the summer of 2023. However, after announcing the winners of Round 3.1 on 30 December 2022, it took eight months for the administrative contract negotiations. Announcements regarding rules for Round 3.2, including a date for auctions have yet to be released despite much speculation.

This does not come a good time for the Taiwanese market, where confidence in the burgeoning OSW industry has dwindled significantly over the past year. This has resulted in internationally renowned developers withdrawing from Round 3.1 bidding, as well as the subsequent announcements of developers exiting the Taiwanese offshore wind energy market altogether. To make matters worse, one large Round 2 project with 1GW capacity slated for 2024/25 has still not passed its financial investment decision milestone. This has created a prevailing sense of pessimism in the market brought about by several factors including increased development costs, unappealing policy, and continued financing struggles. Such factors may be symptomatic of an ongoing ‘domino effect’ in the industry where the combination of delays in implementation of feasible policies, overburdening government and construction delays are compounding difficulties and delaying the OSW rollout. This also means that the OSW sector in Taiwan has not been able to develop a strong resilience, which makes it especially vulnerable to global developments.

The ‘domino effect’ of 3.1

Following the award of Round 3.1, project owners still face many stumbling blocks that might upend their final investment decisions. Those are primarily related to supply chain and financing considerations. This is especially so in the Taiwanese market, which has a shorter construction season, due to challenging weather conditions in the Taiwan Strait. The Ministry of Economic Affairs’ (MOEA) delay of Round 3.1 will potentially set projects back an entire construction season, further delaying Taiwan’s rollout of green energy. Such patterns of delays and on-the-fly policy changes have compounding effects that impact projects later in their life cycles, creating problems and bottlenecks for the entire pipeline and supply chain. Such issues have been in part responsible for industry uncertainty related to overly complicated permitting and consenting processes, supply chain, infrastructure availability, localisation, financing, and ultimately in unmet energy targets.

As we have already seen, a delay of Round 3.1 has led to the further delay of Round 3.2. Current public discussions have indicated the possibility to include the unused 665MW capacity from Round 3.1 in the upcoming auction. While this sounds promising, it may further complicate uncertainty amongst interested bidders and within the supply chain.

Although an additional 2.3GW of added capacity means Taiwan’s OSW energy capacity could reach 8GW by 2027, (5.7GW is already awarded up to 2025), there are several factors which may delay or altogether prevent successful buildout of these projects. Currently, as we look towards Round 3.2, the policy target of 13.1GW by 2030 seems increasingly unlikely.

Related challenges based on current market conditions include:

1. Inflation and high interest rates in the global market remain a challenge for the foreseeable future. Simultaneously, Taiwan's local supply chain costs remain high, preventing Corporate Power Purchase Agreement (CPPA) prices from being attractive for the private market. The financial models of Round 3.1 are already stressed and can easily fall victim to any smaller unfavourable shifts.

2. Uncertainty surrounding the newly implemented credit guarantee mechanism in Taiwan, primarily on whether it will be accepted by domestic and foreign banking groups, and how many companies meet the relevant qualifications.

3. If Round 3.2 regulations are more attractive in terms of cost profiles and increased size, Round 3.1 projects might forfeit their development rights or Round 3.1 projects might rely on more capacity awarded during Round 3.2 to really go ahead.

4. International lenders still have a high participation rate in the market, caused by reluctance of local financial institutions to invest, which may raise subsequent financing difficulties for new projects.

5. Extended delays in Round 2 will lead to further bottlenecks for Round 3.1 projects, impacting their ability to be constructed within the given timeframe and exposing them to penalties and cost overruns that may jeopardize the projects’ financials.

While the deposit for the administrative contracts is relatively high, factors such as the ones listed above may mean that a project’s development will become unviable, leading to abandonment of the gird awards, further delaying fulfilment of Taiwan’s energy goals and hampering the further development of a robust and sustainable supply chain. The government will need to be more supportive in backing up projects, a position they so far have only taken incremental steps towards. There still needs to be more effort to support, for example Taipower acting as the wholesaler for those projects by offering free market prices or for example waiving onerous cost items such as leveraging the responsibility for reserve power margins on renewable energy developers.

Deja-vu? Will Round 3.2 be an uncompetitive auction again?

Taiwan is running out of available space for offshore wind farms within its territorial waters (12 nautical mile zone). To address this issue, the MOEA has from the beginning of Round 3 chosen to create increased competition for developers, by allowing multiple overlapping projects to apply in the same area, and in Round 3.1 by restricting the awards to 500MW per owner.

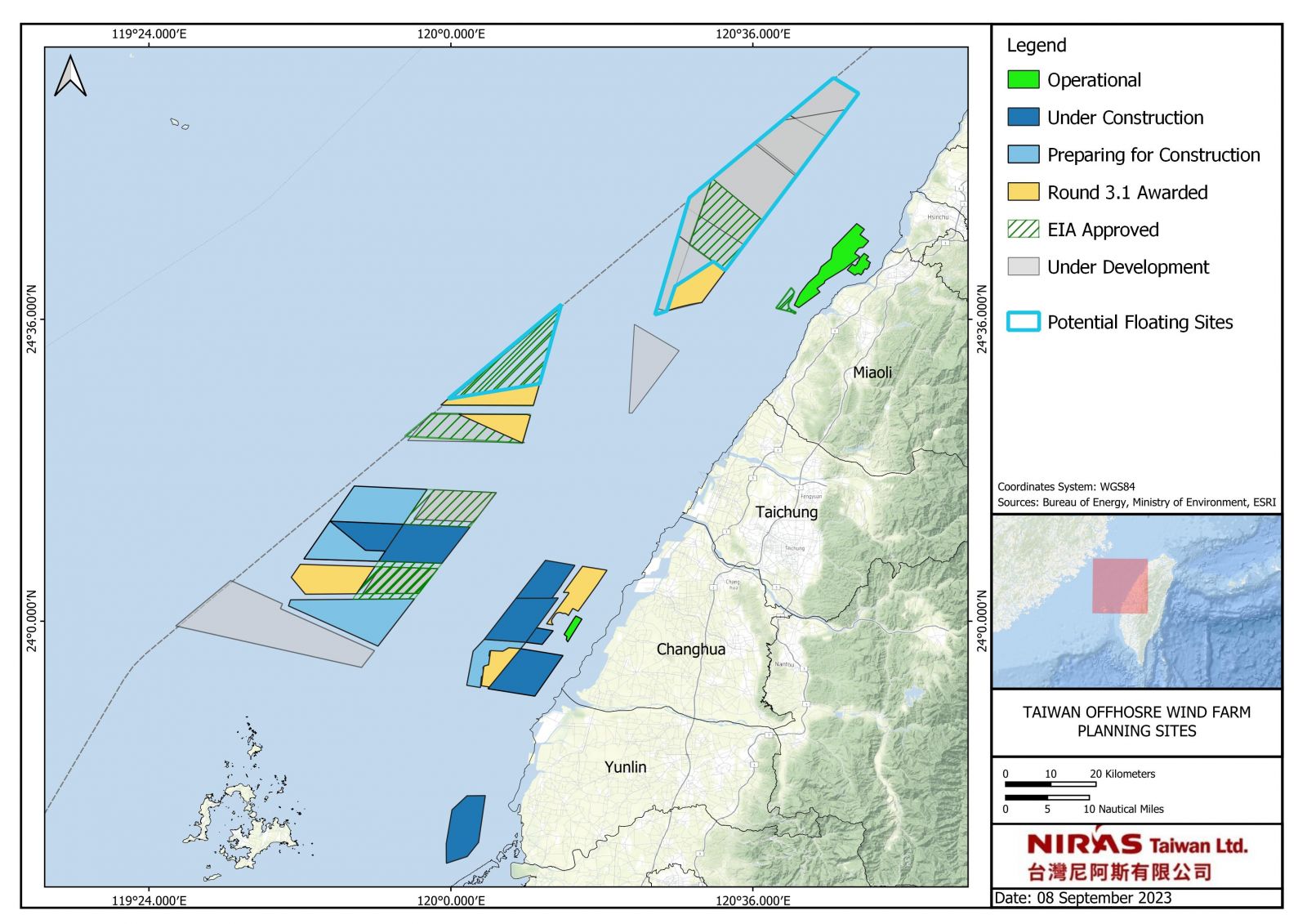

An overview of current projects from Round 1 to Round 3

Round 3.2 will likely prove to be the last round for fixed bottom offshore wind under the current planning regime. Furthermore, the anticipated 3.665 GW might not be fully available for bidding. All the available fixed bottom projects under development are south of the middle of Miaoli as highlighted in grey and green in the map above. Sites that have included floating wind in their development activity plan are framed in turquoise. The key to attract enough competition will probably only lie in increasing the awards from 500MW upwards, possibly to 1GW in an effort to keep developers’ skin in the game and attract as many bidders as possible. Currently six developers have signalled their interest to take their projects forward but at least three of them would essentially be competing for the same areas. Of these, some of the projects that have been lodged with the Ministry of Environment (former EPA) have not yet received their conditional Environmental Impact Assessment (EIA) approvals. Although this could potentially increase the field of participants, with multiple owners bidding on one area, only one project would add to additional capacity. As the government has chosen an aggressive negotiation tactic to force their hand by threatening to penalise those not signing their administrative contracts, at least one developer is likely to refrain from participating in further auctions. Conversely, another developer has signalled its intention to re-join the auctions, should the framework regulations be greatly improved.

A change in the permitting process could potentially increase restrictions to wind farm size for already approved projects. This increase in size limit would change the trajectory of a couple of projects that had already been approved for Round 1. They could potentially up their energy output with a lower footprint, as turbine capacity has now jumped from 6MW to up to 20MW per turbine. But it is unlikely that regulations will be softened to do this via a differential EIA process without restarting the process, as is common practice for all energy projects in Taiwan.

What to expect in Round 3.2

Regardless of its challenges, Taiwan’s OSW market maintains its position as an important market in APAC region coming out of Round 3.1. Looking ahead to Round 3.2, it is likely that the government, in response to Round 3.1, will introduce further policy changes to support the OSW sector, that will relax overly rigid localisation regulations, and introduce a national credit guarantee mechanism that will further support the CPPA market.

Although it is still the subject of speculation, based on recent discussions, it is currently looking likely that regulations for round 3.2 may allow developers to choose their own localisation items within the required scoring system for localisation. This would mark a major step-change from the rigid localisation prescription that was focusing on specific items. The relaxation of localisation requirements would undoubtedly be positive for developers, as associated costs in Taiwan’s local supply chain are higher than in international markets. Such a change in rules would allow developers to select items where the local supply chain is already mature, lowering prices and making the Taiwanese market more competitive on an international scale.

Also included in the conversation for round 3.2 is an increase in the upper limit of project capacity per wind farm to 1GW. According to information disclosed by the MOEA through press channels, round 3.2 capacity limit for projects may be linked to localisation commitments. In other words, higher levels of localisation could result in higher prioritisation for development right ranking and allocation of more capacity. But this could also create a prisoner’s dilemma for the participating developers, as they will see themselves outcompeting each other for resources and ultimately might need to expand their targets to new players or less experienced providers.

Whether local suppliers can seize this opportunity amidst this wave of regulatory adjustments can be seen as a midterm test for Taiwan's supply chain after years of preparation. As Taiwan's OSW power market matures, the supply chain needs to be moving toward liberalisation and open competition. This will be especially important as Taiwan will run out of suitable locations for fixed bottom projects and local companies will need to look for opportunities overseas to remain in business.

Solidifying Taiwan’s pipeline: Holistic marine spatial planning

If Taiwan wants to achieve its net zero energy transition targets by 2050 it will need to reform its marine spatial planning regime. As all the good locations for fixed bottom projects are already close to being used, a first step was taken with the reform of the Renewable Energy Development Act this year allowing OSW development beyond a 12 nautical mile zone. However, there is still a lack of a clear approval pathway and alignment with other marine users and their respective authorities in that area. Those projects will obviously be further away, making them more costly to develop. An orderly development framework would allow for lower costs and avoid problems that have plagued Taiwan from the very beginning of its zonal planning approach back in 2016 and in the government’s near total hands-off approach in site selection for Round 3 so far.

Outlook

Coming out of the award phase from Round 3.1, Taiwan’s OSW market continues its forward momentum despite industry pessimism and uncertainty. There is hope that a change in regulations for Round 3.2 may ultimately lead to reduced energy prices, as a result of greater economies of scale through larger awards, a more competitive supply chain in tandem with a positive outlook for Taiwan’s overall industry that has already created thousands of high paying of local jobs. This all still stands on shaky ground, and the stability of the industry and renewable energy in general will not be sustainable without better policy. Taiwan may already have seen its ‘heyday’ for offshore wind, but there is still hope for growth and stability as the market continues to mature going forward.

Jason Wang is a Senior Economist for NIRAS, a Danish multi-disciplinary engineering company, focused on energy policy and market forecast consultancy for clients and supporting NIRAS’ efforts in Environmental Social and Governance (ESG) offerings in the APAC region.

Raoul Kubitschek has worked in Taiwan’s renewable energy sector since 2008 and is currently the Taiwan Country Manager for NIRAS. He is concurrently Co-Chair of the ECCT’s Energy and Environment committee.

James McCatherin is a Consultant working for NIRAS. He supports social & political considerations for Offshore Wind as well as Environmental Social and Governance (ESG) in Taiwan and the APAC region. His background is in International Development and Political Science.