Economy & Business

Correspondent banking

Correspondent banking - when banks onboard banks - happens far more often than customers of retail banks might imagine

By Paul Shelton

In an earlier article, In defence of Taiwanese banks I strove to articulate the account opening process with Taiwanese banks for those (perhaps new to Taiwan) who felt that the process was overly heavy on documentation. I pointed out in that article that Taiwanese banks are bureaucratic but their account opening procedures were very much in line with most banks internationally. Onboarding a client, retail or commercial, is part of the Know Your Client (KYC) procedures that banks follow. Banks need to know about you, about your business, your employment, the likely nature of your banking transactions. They will rate you based on their assessment of risk, usually, high, medium, or low and they will periodically review your account according to that risk rating. Banks will monitor your activities and they may even question certain transactions (especially inflows of funds).

Banks will also monitor you against their “bad guys” lists and their sanctions lists – in these times of geopolitical upheaval this monitoring is no doubt running at absolute capacity in some jurisdictions. You don’t want to be on one of these lists!

The average retail client tends to think of their banks (let’s say for the sake of argument you only bank with one institution) as being a one-stop shop. This one bank does everything for you from taking deposits, allowing withdrawals, providing loans and credit cards. In this international world in which we exist our bank also transmits funds both in local and international currencies for us.

However, this is simply not the case. Banks and/or their individual branches are not one-stop shops for all services. Perhaps they give that impression but, behind the scenes, it is a very different world.

Put simply, banks rely on other banks to provide them with services that they either don’t provide or would find it uneconomic because of their size and scale to provide. Welcome to the somewhat complicated world of correspondent banking!

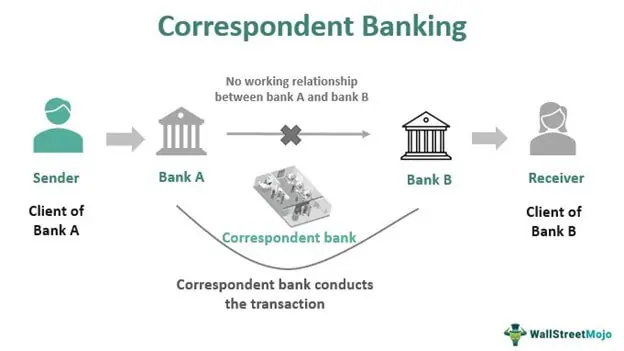

Correspondent banking involves an account established by a banking institution to receive deposits from, make payments on behalf of, or handle other financial transactions for another financial institution. Correspondent accounts are established through bilateral agreements between the two banks.

The diagram below provides as clear an example of a basic correspondent banking relationship.

In the above example, the Sender wants to send some money to the Receiver at a different bank. In this instance two banks are required to connect with each other (it usually involves a foreign entity) and, as noted above, there may be a lack of prior relationships with those banks or a lack of resources. As a result, the banks pay third-party institutions to participate in their transactions. It benefits the correspondent entity (which earns revenue from charges they apply for serving as an intermediary between the two unconnected banks). Perhaps this might also help explain why international transmissions can be perceived as costly and slow.

The main services provided by correspondent bank include:

- Wire transfers (probably the most common)

- Transaction settlements

- Trade finance (which may in multiple correspondent banks in one transaction)

- Currency exchange (a service that a lot of banks these days are increasingly reluctant to provide, perhaps because it is seen as too burdensome for the effort)

- Treasury services

- Check clearing

- Managing international investments (i.e., investments that are made outside the domestic market of the investor)

- Collecting documents internationally – a rarely offered or used service.

Correspondent banks will most often be involved in the transfer of funds, and accounts handling the fund transfer are called ‘Nostro’ (simply meaning ‘ours’) and ‘Vostro (simply meaning ‘yours’). The respondent bank refers to their account with the correspondent bank as Nostro (ours), and the correspondent entity refers to the account for a respondent entity with them as Vostro (yours).

Until the last couple of years, the major network used to expedite this system of transfers and payments (global remittances) was the SWIFT network. SWIFT was founded in 1973. The acronym stands for the “Society for Worldwide Interbank Financial Telecommunication” and it is a Belgian cooperative society providing services related to the execution of financial transactions and payments between banks worldwide. However, as the world of FinTech and payment systems continuously evolve, SWIFT faces much stiffer competition and customers wishing to make global remittances have more options when making remittances.

There are clear benefits to a correspondent banking arrangement or relationship. A correspondent banking relationship enables the respondent bank to shop for services from the correspondent bank and allows a bank to provide their clients with services in a region where the respondent bank doesn’t have a branch or presence. This correspondent banking relationship provides benefits such as:

- An increase in clients

- An increase in revenue

- Gaining a competitive advantage by offering services that are not provided by its competitors

- A possible reduction in the cost of geographical extension of the banking organisation (Banks don’t always want to open small expensive branches in remote locations. It simply makes no economic sense. Hence the use of a correspondent bank. The bank gets to keep or even expand its existing customer base and not lose customers when they need international operations. Trade finance is a classic example of the type of business requiring correspondent banks).

Correspondent banking relationships are essential in the global payment system and vital to international trade (and we know how reliant Taiwan’s economy is on exports/imports), including with emerging markets and developing economies. But the reliance on correspondent banking relationships provides potential scope for money laundering/terrorist financing.

The existence of money laundering and terrorist finance risk brings organisations such as the Financial Action Task Force (FATF, also known by its French name, Groupe d'action financière, is an intergovernmental organisation founded in 1989 on the initiative of the G7 to develop policies to combat money laundering and terrorist financing) very much front and center into the world of correspondent banking.

FATF publishes recommendations that require financial institutions to identify and manage the risks associated with correspondent banking business relationships and to apply specific due diligence measures when they are conducted on a cross-border basis. When FATF ‘recommends’ it is usually seen as something more concrete than a simple recommendation. Failure to implement FATF’s recommendations can have a material impact on a financial institution or the jurisdiction in which the financial institution is regulated.

However, in recent years, some financial institutions have increasingly decided to avoid, rather than to manage, possible money laundering or terrorist financing risks, by terminating business relationships with entire regions or classes of customers.

This so-called 'de-risking' practice has negatively impacted correspondent banking. De-risking is not in line with the FATF recommendations, and is a serious concern to the international community, including the FATF and the FATF-style regional bodies. De-risking can result in financial exclusion, less transparency and greater exposure to money laundering and terrorist financing risks by forcing banking customers to seek other perhaps less controlled means of transferring funds or transacting international business.

Accordingly, FATF clarified to the international financial universe that financial institutions should adopt the application of the risk-based approach to correspondent banking relationships. But what does “risk-based” approach mean? For example, some financial institutions seemed to believe that they needed to conduct customer due diligence on each individual customer of their respondent institutions’ customers. This would be a task of unimaginable difficulty. FATF therefore provided additional guidance and highlighted that not all correspondent banking relationships carry the same level of money laundering or terrorist financing risks. Hence, any enhanced due diligence measures must be commensurate to the degree of risks identified.

This additional guidance did help reduce some of the noise in the markets. FATF’s original guidance in 2016 on correspondent banking alone, ran to some 22 pages of extremely detailed advice but even then, as we’ve noted above, further guidance and elucidation was required.

But in the world of correspondent banking, it is not FATF that is seen as the paramount global body. The real international driving force is the Wolfsberg Group. Founded in 2000, it is a non-governmental association of thirteen global banks. Its goal has been to develop financial industry standards for anti-money laundering, know your customer and counter terrorist financing policies. The influence and authority of the Wolfsberg Group as an association of just thirteen global banks should not be underestimated and hopefully the following will demonstrate their importance and global reach.

Importantly, in October this year the Wolfsberg Group published its updated Financial Crime Principles for Correspondent Banking. This document updates the 2014 version and provides guidance and best practices for banks, draws a distinction between correspondent relationships and correspondent banking activity, addresses entities other than banks who have correspondent relationships, and incorporates revised Frequently Asked Questions that were previously a separate document.

The Wolfsberg Group’s principles detail risk-based due diligence measures that, when undertaken, allow the correspondent bank to assess the profile, customer base and financial crime programme of its respondent customers. The Wolfsberg Group believes that these principles assist correspondent banks in developing a programme that includes a fulsome assessment of the risks presented in correspondent banking relationships and enables a comprehensive review of those risks as they apply to the respondent banks.

For respondent banks receiving services, the Wolfsberg Group document provides an understanding of the expectations they may encounter when requesting a correspondent banking relationship. The updated document defines the activity that presents the most risk and introduces the concept of a defined risk appetite for correspondent banking activity. It also provides factors to be considered during the periodic review and ongoing management of correspondent banking relationships to determine if the relationship continues to be within the risk appetite.

Whilst the update is certainly important, the Wolfsberg Group provides even more granular assistance to financial institutions involved in correspondent banking. At the start of this article, I noted how some retail banking clients feel that opening an account is now simply too complicated and too bureaucratic. But the following will reveal just how rigorous financial institutions are advised be when entering into correspondent banking arrangements. That rigor is to be found in the Wolfsberg Group’s Correspondent Banking Due Diligence Questionnaire (the CBDDQ). The CBDDQ is some 20 pages of questions with 36 questions in total (many with detailed subsections) and they cover the following areas:

- Entity & ownership

- Products & services

- AML, CTF & sanctions program

- Anti-bribery & corruption.

The Wolfsberg Group advises financial institution that the CBDDQ is required to be answered on a Legal Entity (LE) level (which for some financial institutions may mean multiple versions are required) including any branches for which the client base, products and control model are materially similar to the LE head office. This questionnaire should not cover more than one LE.

Each question in the CBDDQ needs to be addressed from the perspective of the LE and on behalf of all of its branches. If a response for the LE differs for one of its branches, this needs to be highlighted and details regarding this difference captured at the end of each sub-section. If a branch's business activity (products offered, client base etc.) is materially different than its Legal Entity’s head office, a separate questionnaire should be completed for that branch.

The Wolfsberg Group then advises that when an LE completes the CBDDQ, that copy must have a completed and signed declaration statement. This declaration statement requires the signature of the global head of correspondent banking, or equivalent, and the money laundering reporting officer, or equivalent of each LE. The inclusion of the business into the declaration statement acknowledges the business manager’s accountability for correspondent banking risks.

To aid this mammoth undertaking by respective financial institutions, the Wolfsberg Group also provides a 20-page completion guidance to the CBDDQ.

The Wolfsberg Group is quite candid in its insistence that the CBDDQ and the completion guidance are meant to drive consistency through the correct interpretation of the questions, ensure the quality of the data collected is both accurate and consistent and place the international engagement in correspondent banking on a firm footing.

Banks often have teams that are fully dedicated to the on-boarding procedures for correspondent banking and at the very least it requires professionals with a deep understanding of correspondent banking. It should be noted that the CBDDQ is sometimes just regarded as the baseline of the KYC done between banks. If the activities carry particular risks, it is quite normal for the onboarding bank to request further information – in particular, information concerning the client bank’s AML/CTF programme. The request for additional information adds another layer of complexity to correspondent banking but the management of risk is paramount in today’s heavily regulated banking environments.

So, how do Taiwan’s financial institutions function within the correspondent banking world? Well, no surprise there for guessing that they are quite active. The Financial Services Commission (FSC) requires Taiwanese banks to perform proper due diligence (i.e., the CBDDQ) on offshore banks with which they wish to conduct business. The regulations are quite clear on the following points:

- Banking businesses and other financial institutions designated by the FSC shall establish specific policies and procedures for correspondent banking and other similar relationships, including –

- Gathering sufficient publicly available information to fully understand the nature of the respondent bank’s business and to determine its reputation and quality of management, including whether it has complied with the Anti-Money Laundering and Countering Terrorism Financing regulations and whether it has been investigated or received regulatory action in connection with money laundering or terrorist financing

- Assessing whether the respondent bank has adequate and effective AML/CFT controls

- Obtaining approval from senior management before establishing new correspondent bank relationships

- Documenting the respective AML/CFT responsibilities of each party

- Where a correspondent relationship involves in “payable–through accounts”, the banking business shall be required to satisfy itself that the respondent bank has performed customer due diligence (CDD) measures on its customers who have direct access to the accounts of the correspondent bank, and is able to provide relevant CDD information upon request to the correspondent bank

- The banking business is prohibited from entering into correspondent relationships with shell banks and shall be required to satisfy itself that respondent financial institutions do not permit their accounts to be used by shell banks

- For a respondent bank that is unable to provide the aforementioned information upon request, the banking business or other financial institutions designated by the FSC may decline the respondent bank’s application to open an account, suspend transactions with the respondent bank, file a suspicious ML/TF transaction report or terminate business relationship

- The aforementioned provisions are also applied to the respondent bank that is a foreign branch or subsidiary of the banking business or financial institutions designated by the FSC.

As usual, all very clear and well documented by the FSC but the real work is between the banks at the heart of the correspondent banking relationship.

I’ve not been able to obtain full data on the number of Taiwanese banks that engage in Correspondent Banking, but I was able to view a list that detailed 11 major Taiwanese banks being active as of June 2019. I would sincerely doubt that this number has decreased. I would in fact expect an increase and, as evidence of that, I was also able to identify one bank from the Philippines that was currently conducting correspondent banking business with 19 banks in Taiwan (no doubt to help service the very active trading relationship between Taiwan and the Philippines).

So, there is the world of correspondent banking, large, complex but overseen not only by the local regulators but actively supported by international organizations such as FATF and the Wolfsberg Group. Perhaps now that the borders are open again and international trading actively resumes or indeed increases, we will witness a growth in correspondent banking in Taiwan.

Paul Shelton is a consultant with 30 years of experience in the international financial services and related industries with skills in all aspects of legal and financial crime compliance and regulatory relationship advisory and management.