Economy & Business

Taiwan's battery sector

Taiwan’s battery sector has surged on the Covid-fuelled consumer electronics boom. Electric vehicles and energy storage will drive future growth

By Tim Ferry

Azizi Tucker, formerly with Tesla and co-founder of Taipei-based Xing Mobility, maker of industrial electric power trains, says that his recent efforts designing innovative electric vehicles (EV) have run into an unexpected roadblock: he’s having difficulties sourcing the battery cells he needs.

“Globally, battery cells are at record production output and consumption, and they are just hard to get,” he observed. “It’s painful, but everyone is going through the same thing.”

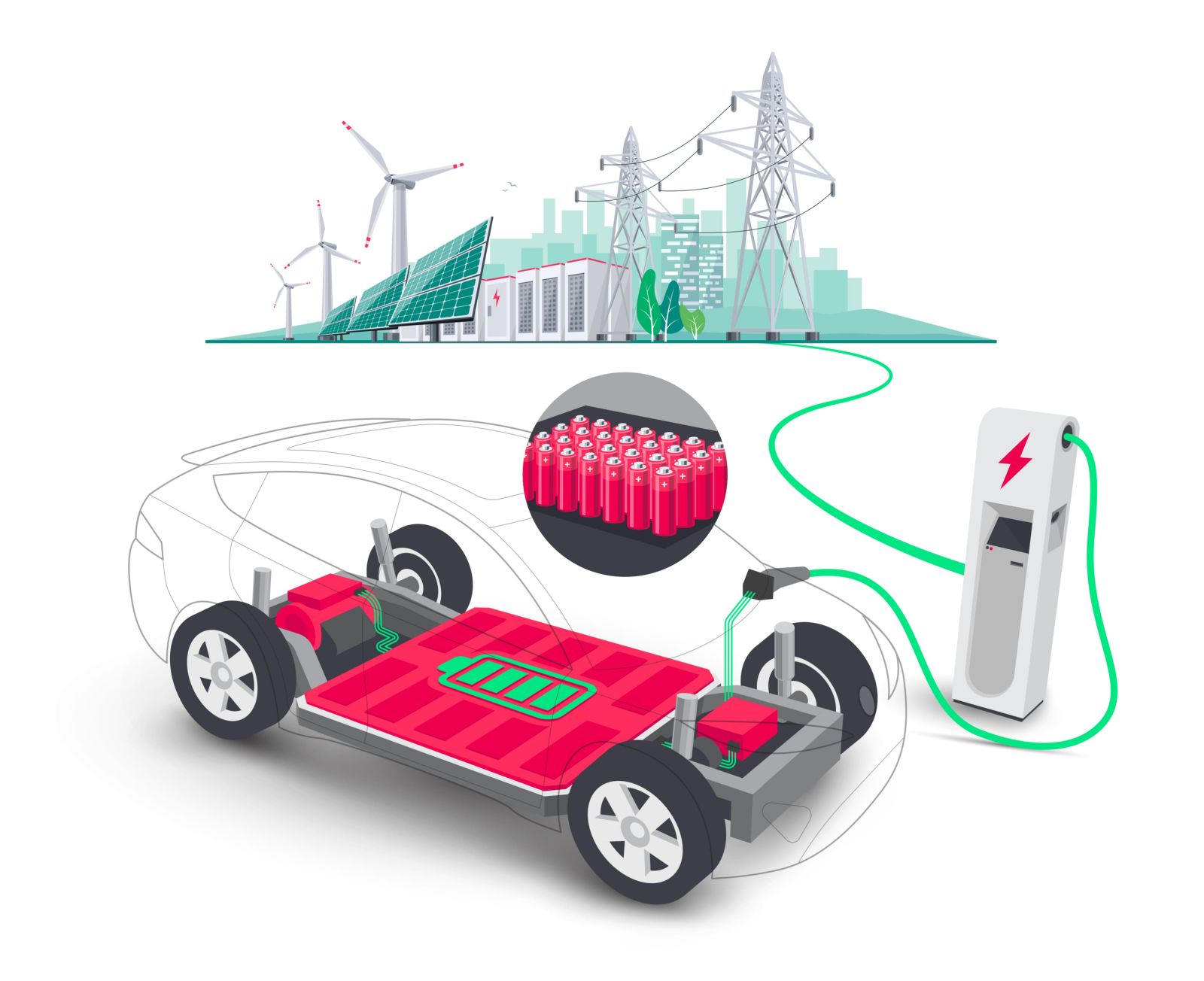

The market for rechargeable batteries has exploded recently, particularly amid the global pandemic that saw surging demand for mobile electronics such as smartphones and notebook computers, but also in tandem with the rise of EV markets and energy storage systems (ESS) to complement renewable energy. This surging demand has resulted in strong growth for the world’s battery makers, including those in Taiwan, and strong competition among the industry’s players.

“The Covid-19 pandemic resulted in very positive and optimistic demand for batteries and has benefitted Taiwanese manufacturers, especially for the battery pack manufacturers,” observed Dr Mark Lu, researcher at Taiwan’s premier research institute, the Industrial Technology Research Institute (ITRI). “This has created a new record for their operating revenue in the past several quarters.”

The battery sector is divided into “primary”, which are disposable batteries, and “secondary”, which are rechargeable. The primary sector now makes up less than 14% of the worldwide US$103.76 billion market for batteries in 2019, according to research provided by ITRI. For the secondary market, traditional lead-acid batteries, such as those found in conventional internal combustion driven autos, backup power for industrial and commercial facilities, electric bicycles, and uninterrupted power supply (UPS) systems, still comprise the largest share of the market, coming in at US$47.8 billion, or 46% of the total market.

But while lead-acid batteries remain on top for now, growth remains in the lithium-ion battery segment, which stood at US$38.85 billion in 2019, or 37% of the market, and is gaining fast. US-based market research firm OG Analysis predicts that the market for lithium-ion batteries will see a cumulative annual growth rate (CAGR) of 14.6% to reach US$91.9 billion by 2026, while ITRI sees the lithium-ion battery sector growing to US$52.56 billion by 2022, a 35% gain over 2019.

Lithium-ion batteries are gaining ground due to their higher energy density, minimal maintenance, and good energy-to-weight ratios as well as high open-circuit voltage.

A battery is comprised of multiple cells, each of which consists of a single anode and cathode separated by an electrolyte, which produces voltage and current. A lithium-ion battery uses lithium as the anode and may use any number of other materials for a cathode, including cobalt-oxide, iron phosphate, manganese oxide, nickel-manganese-cobalt, and nickel-cobalt-aluminum oxide. Around 95% of the world’s lithium-ion battery cells are produced in Japan, South Korea, and China, with Taiwan playing only a minor role.

“Because of the sourcing issue with the raw materials, large scale is necessary and small-scale manufacturers tend not to make it,” observed Tucker.

Taiwan does boast 20 companies making cells, including E-One Moli, Pishiang, Amita, and Synergy. Lacking the economies of scale, these companies are at the high end of price ranges but offer quality products with local service while avoiding import tariffs that can drive up competitors’ prices.

Taiwan has a much larger footprint in the battery pack assembly sector, with US$4.16 billion in sales in 2019, amounting to nearly 13% of worldwide market share. Competitors in this segment include Simplo, DynaPack, Celxpert, WELLDONE, Delta, and Foxlink. Taiwan’s links to global IT supply chains have positioned the battery pack assemblers to snare significant market share, and ITRI data reveal that Taiwanese firms have over 60% of the worldwide notebook battery pack assembly, more than 45% of the tablet computer battery packs, and 11% of the power tools segment.

Taiwan’s battery makers are looking beyond consumer electronics, though, and towards the EV and power train systems segments, which were already estimated to be worth US$71 billion in 2019 by Fortune Business Insights, while market analytics firm Markets to Markets sees 25% CAGR in EV sales through 2025. As the EV sector is driven by government policies that offer subsidies, ITRI’s Lu says that this market is attractive not only for its growth but for its high profit margins.

Taiwan does not have a large presence in manufacturing automotive EV batteries but is gaining ground in smaller EVs such as E-bikes and E-scooters. These sectors are likewise being heavily pushed particularly in Europe where public transportation is now out of favour with a Covid-wary public.

Lithium-ion batteries will play an increasingly large role in helping balance power grids that are struggling to incorporate increasing amounts of intermittent renewable energy.

Pushing for greater uptake of energy storage systems (ESS) in Taiwan and abroad

Paul Chien, whose family has been in the battery industry for generations, started Cosmos Infinity to create high-voltage ESS systems for different demands, including helping power utilities to manage their grids. Cosmos Infinity is making inroads into Japan’s newly deregulated power market which has enabled retail players to provide power purchase agreements (PPA) to household consumers with ESS systems.

Consumers can either install a solar system to charge the ESS or charge it off the grid during the night when rates are low, and then sell it back to the utility during midday when rates are high. For consumers, this both reduces the basic rates they pay to the power utility while also reducing their rate per kilowatt hour (kWh). For the utility, it helps them to balance the grid without resorting to directly purchasing ESS.

He does not see a similar market developing in Taiwan, however, due to Taiwan’s extremely low power prices. The average price for power in Taiwan is NT$2.6/kWh (US$0.09/kWh), while in Japan, which is among the top six countries for electricity prices, the average rate is three times higher, at the equivalent of US$0.27/kWh.

“ESS in Taiwan really doesn’t make sense,” he observed. “But in Japan, consumers can lower their electricity price almost right away.”

Chien said that in the ESS market, Taiwan can compete not only on price but on the quality of its battery management systems (BMS).

“We have the hardware now, but now we need to focus on the software too,” he said, noting that this is critical for enabling ESS to be instrumental in balancing the grid. “Basically, it's energy trading.”

Meg Lin, Associate Research Fellow at the Research and Development Center for Green Energy at the Taiwan Institute for Economic Research (TIER) said that the government is looking into regulations to incentivise the transition of safety backup power systems from lead-acid batteries and diesel generators to lithium-ion batteries and fuel cells.

“We have the market, but we are still lacking the regulations,” she said.

Cleaning up the industry

The concentration of the industry into so few countries as well as the need for materials, such as lithium, cobalt, nickel, and others that are not easily found, results in supply bottlenecks and environmental and social problems. As much as 50% of the world’s cobalt is mined in the Democratic Republic of the Congo and is replete with accusations of worker exploitation and child labour. Many of the materials in lithium-ion batteries are subject to wild price gyrations and supply disruptions as well, according to ITRI’s Lu.

Accordingly, ITRI and other universities and research centers are following global lithium-ion battery technology trends towards “Cobalt-free” batteries that deploy less harmful substances. ITRI’s Lu said that Taiwanese companies are working on silicon-anode, solid-state electrolyte battery (SSB), and other revolutionary materials.

“This will be a big challenge, but we are making progress,” Lu said.

Tim Ferry is an American journalist covering Taiwan’s energy transition