Economy & Business

The future of work

Seismic shifts are taking place in how work gets done, but can society handle them and how will Taiwan adapt?

By Mike Jewell

The ever-evolving way of working

There have been lots of changes in the way people work in my 40 years in the business world. Those of a similar vintage to me will recall desks littered with papers, staplers, notepads, pens, pencils, paper clips and so on, but no sign of a computer. When I started out in 1979, A.C. Nielsen in Oxford had one computer, the size of a small house. Phone calls went through the switchboard and, when travelling, we kept in touch with base by shovelling bags of coins into public phones. Letters, reports, contracts, invoices, all typed, with liberal use of Tipp-Ex and correction ribbons, were carried to clients by the Post Office, while urgent messages went by telex. Presentations were created manually and delivered on acetates and OHPs (overhead projectors, for the Millennials among you). One of the most prized and jealously guarded items of office equipment was a set of coloured acetate pens.

Then came facsimiles (i.e. faxes), which allowed documents to be sent via telephone lines, although sending a 100-page report was always fraught with anxiety, waiting for the inevitable break in the line, wondering whether the receiving office had enough paper and ink in their machine and dreading the call that said “we got the first six pages!” Next, we had “BB calls” and Blackberry’s and the personal computer arrived, with built-in word processing and spreadsheets and – joy of joys – graphics packages. Hello PowerPoint!

Smartphones came soon after and, with the ubiquity of the internet, we have instant connectivity 24/7, at least in those areas of the world with access to 4G and 5G.

Technological advances and automation have brought significant changes to many areas of commercial activity. In the pursuit of ever greater efficiency and lower operating costs much manufacturing has seen manual labour replaced by robots that don’t take sick leave or coffee breaks or holidays, while, in many parts of the world, agriculture has also become highly mechanised.

And still more change lies ahead, as AI solutions are embedded ever more widely across the global commercial environment.

Despite all this, though, how much has work really changed? Quite simply, business owners employ people to do certain tasks in a certain location for a number of hours each week. They provide them with the facilities to carry out those tasks and (hopefully) pay them for completing them. It’s been that way since the industrial revolution.

Changes are happening, of course, and potentially quite radical ones – just look at the emergence of the gig economy and of the “New Work” movement in Europe – and the pace of change is increasing exponentially but, for the most part, the overall pattern has stubbornly endured – until 2020.

Enter Covid-19 – sudden total global disruption and a new dynamic in labour markets

In response to the pandemic and the inadequate efforts of so many governments in trying to rein it in, employees and employers of necessity embarked on the biggest ever experiment in adopting new ways of working. Writing in Commonwealth Magazine recently, Florian Rustler, founder of Creaffective, gave a concrete example of how the pandemic instantly brought about a significant change in one company’s working practice.

“A customer of ours, a large bank in Germany, was discussing for over ten years to allow people to work from home, at least in part. For ten years there were repeated arguments why that would be impossible from technical, procedural and compliance perspectives. Thus, nothing happened.

Once Germany went into lockdown in March 2020, within 48(!) hours 7,000 people were allowed and equipped to work from home. No major problems occurred. So, the reason why work from home was impossible in the past was never a technical one. It was a cultural one. People could not and did not want to imagine that it was possible.”

As it becomes increasingly clear that Covid-19 will not be put back in its bottle any time soon, much thought is being given to trying to determine how much of the emergency response will become SOP, the so-called “new normal” and, more importantly, in trying to anticipate all of the implications for society.

The future of work after Covid-19”, produced by McKinsey Global Institute (MGI), offers some well-researched and thought-provoking insights, based on observations across eight diverse labour markets – the US, China, Japan, India, the UK, France, Germany and Spain.

The most significant result of the Covid outbreak is the recognition of the need to limit physical closeness in the workplace, to reduce the spread of the disease. There have been damaging pandemics throughout history, but this is perhaps the first time that business has begun to look seriously at ways of reducing social interactions as a long-term component of health and safety strategy and it is likely that business models will shift dramatically, with major consequences for the overall structure of industry and even society as a whole.

MGI take this principle as the starting point for their analysis. They segment occupations according to their proximity to coworkers and customers, the number of interpersonal interactions involved, and their on-site and indoor nature, identifying ten different work arenas and they conclude that jobs in work arenas with higher levels of proximity are likely to see greater transformation after the pandemic.

According to MGI, Covid-19 has given massive added impetus to three existing broad workplace trends.

- Remote work and virtual meetings are likely to continue, albeit less intensely than at the pandemic’s peak

- E-commerce and other virtual transactions are booming.

- Covid-19 may propel faster adoption of automation and AI, especially in work arenas with high physical proximity.

Some of the likely consequences arising from these trends:

- If 20-25% of the workforces in advanced economies work from home 3-5 days a week (MGI’s forecast of the ceiling for remote working without any loss in productivity), this could prompt a major shift of individuals and companies out of large cities into suburbs and small cities. Demand for restaurants and retail in downtown areas and for public transportation may decline as a result.

- Some companies are already planning to shift to flexible workspaces after positive experiences with remote work during the pandemic, a move that will reduce the overall space they need, leading to an oversupply of office property.

- Remote working and the parallel rise of videoconferencing will reduce the profitable business travel sector by about 20%, forcing airlines to adopt a different operating model and severely affecting employment in airports, hospitality, and food services.

- The move to digital transactions is propelling growth in delivery, transportation, and warehouse jobs. In China, for example, e-commerce, delivery, and social media jobs grew by more than 5.1 million during the first half of 2020. However, traditional brick-and-mortar retailers are being forced out of business.

- Under Covid-19, many businesses have turned to automation and AI in warehouses, grocery stores, call centres, and manufacturing plants to reduce workplace density and cope with surges in demand. Two thirds of senior executives, surveyed by McKinsey in 2020, indicated they will continue to invest in automation and AI, resulting in the disappearance of large numbers of jobs.

MGI anticipate that these trends will have most negative impact on workers in food service and customer sales and service positions, as well as less-skilled office support roles. Jobs in warehousing and transportation may increase as a result of the growth in e-commerce and the delivery economy, but those increases are unlikely to offset the disappearance of many low-wage jobs. In the US, customer service and food service jobs could fall by 4.3 million, while new transportation jobs might number only 800,000.

Before the pandemic, net job losses were concentrated in middle-wage occupations in manufacturing and some office work, due to automation, and low- and high-wage jobs grew. Nearly all low-wage workers who lost jobs could move into other low-wage occupations, but the pandemic’s impact on low-wage jobs means that almost all growth in labour demand will occur in high-wage jobs. Demand for workers in the healthcare and science, technology, engineering and mathematics sectors may grow strongly, reflecting increased attention to health as populations age and incomes rise as well as the growing need for people who can create, deploy, and maintain new technologies.

Going forward, more than half of displaced low-wage workers may need to shift to occupations in higher wage brackets that require different, more advanced skills to remain employed.

The challenge of embedding workforce transition

Enabling the transition to the new ways of working is a large and complex process and demands co-ordinated action from industry and from policymakers to make it as smooth as possible and to minimise the likelihood of social problems associated with rising unemployment. There will be an urgent need for a massive programme of education and training to equip the workforce with the necessary skills for the new workplace.

Governments should support businesses by expanding and enhancing the digital infrastructure and should extend benefits and protections to independent workers and to workers working to build their skills and knowledge mid-career or migrating between occupations.

Switching from office-based working to remote working (the concept has already become so firmly established that it already has been awarded its own acronyms – WFA/WFH, “work from home/work from anywhere”) also throws up a host of regulatory issues that had never been thought of when existing labour legislation across the world was enacted. (This area was explored thoroughly by Howard Shiu and Pamela Tsai from Baker McKenzie and Lynn Chen from KPMG during the ECCT HR Forum in March, and the event report can be accessed via the Chamber’s website https://www.ecct.com.tw/2021-ecct-hr-forum/).

As noted previously, WFH/WFA is only applicable to a minority of the workforce, albeit a significant minority, but, according to MGI, there are certain work arenas, such as the computer-based work arena, where as much as 70% of work can be completed effectively from anywhere, provided the communication links are up to standard. Those working in this arena, such as accountants, financial managers, and legal secretaries, do not require special equipment, and most of their interactions with colleagues and other business contacts can be conducted virtually. In most other work arenas perhaps only 5-10% of work could be done remotely.

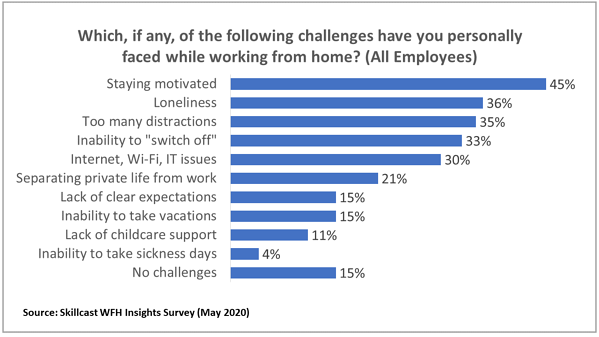

WFA/WFH represents a huge shift in lifestyle for those who adopt it and businesses will need to participate fully in helping their employees adapt to the new reality. Various surveys have been conducted since the onset of Covid-19 to measure how employees are coping with the alternative work environment. The chart below, taken from a survey conducted by Skillcast in the UK in May 2020, provides a typical picture of the frustrations of WFA, with 85% of the nearly 2,000 participants experiencing at least one of the challenges.

“The main challenge I face as a remote worker is isolation. Although, the benefits are that I can more or less work my own hours and from any location, the fact that I work alone is something that I’ve had to overcome. When I worked in an office back in Australia, my colleagues were also my friends. We would socialise often, particularly for that great institution of workplaces around the world: Friday night drinks.”

Diane Lee, freelance writer, and editor

In the HR Forum, Chafic Nassif, from Ericsson Taiwan, discussed how Ericsson is engaging with their employees to help them manage the transition to WFH. Ericsson responded early on in the pandemic by encouraging most of its workforce to work from home. To help employees upgrade their home offices, in addition to digital tools, the company arranged a contract with Ikea and subsidised the costs of desks, ergonomic chairs and desk lights for all of its employees. It has also arranged special leisure activities for employees, such as virtual concerts featuring famous artists.

Nassif believes that WFH has worked well, and an in-house survey revealed that 31% of employees thought they were more efficient when working from home, while 63% said they were just as effective as when in the office. As to how employees are adapting, the majority of employees want to work 2-3 days a week from home, but still come to the office for the rest of the time, suggesting that the personal social interaction of the workplace remains a valuable component of the working experience (as referenced in Diane Lee’s comment). Indeed, almost one third of Ericsson staff claimed they were expressing increased levels of stress, when working at home.

With this in mind, Ericsson (and many other companies around the world in MGI’s “computer-based work arena”) are looking towards a future hybrid work model fusing physical and virtual working. The office premises will remain a focal point for the organisation, but with a reimagined purpose and role, with the design based on employees’ different needs and preferences, rather than roles and function. The offices will be a space where the company comes together to create, collaborate, and socialise.

How will Taiwan embrace the new way of working?

Here in Taiwan, we can feel justifiably proud of how the whole society has dealt with the Covid-19 crisis and the government’s excellent and decisive management, coupled with people’s general readiness to follow the advice of the CECC has meant that we have had to endure very few of the restrictions imposed in so many other countries.

One consequence has been very little change in ways of working. There was some reaction to the pandemic in the first few months of 2020 and some companies introduced WFH practices coupled with split teams and rotational office attendance, but, in the main, these were abandoned after just a few weeks, once it seemed clear that Taiwan wasn’t going to experience widespread domestic disease transmission. By mid-year, working life had largely resumed its conventional path and there is currently precious little evidence of Taiwan business looking to move forward with the rest of the world in adopting new ways of working.

Florian Rustler again, in Commonwealth magazine:

“As a coach, facilitator, and consultant, I regularly interact with larger groups from my clients. In the past these interactions were 95% on site and face to face. Doing this virtually was not even considered an option. Now, the majority of my work happens virtually, with me located in Taipei and my customer groups just anywhere in the world. This happens with all customers except for the ones in Taiwan. They want things on-site ‘because virtual doesn’t really work for this kind of situation’. The same arguments came from European companies until March 2020.”

Unlike Rustler’s German bank client, Taiwan’s businesses have not had change forced upon them and therefore the ultra-conservative attitude of business leaders and resistance to change has not had to do anything differently. According to journalist Daphne Lee, “Taiwan’s work culture is still stuck in its glorious manufacturing days of the 1970s.”

Interviewed in the Taipei Times last June, Christine Chen of Winkler Partners made similar comments:

“In reality, the main obstacle to working from home is not the legal framework but rather Taiwanese business culture and employer attitudes. Almost all of my clients who’ve asked questions about WFH are foreign businesses. I think foreign companies are more open to employees working from home.”

Business owners can counter this by pointing to Taiwan’s robust economic performance throughout the pandemic, but profound and radical change is under way across the rest of the industrialised world and Taiwan’s stubborn adherence to the “old ways” risks it falling behind other countries and at a huge disadvantage in terms of global competitiveness.