Economy & Business

Food & grocery retailing in Taiwan

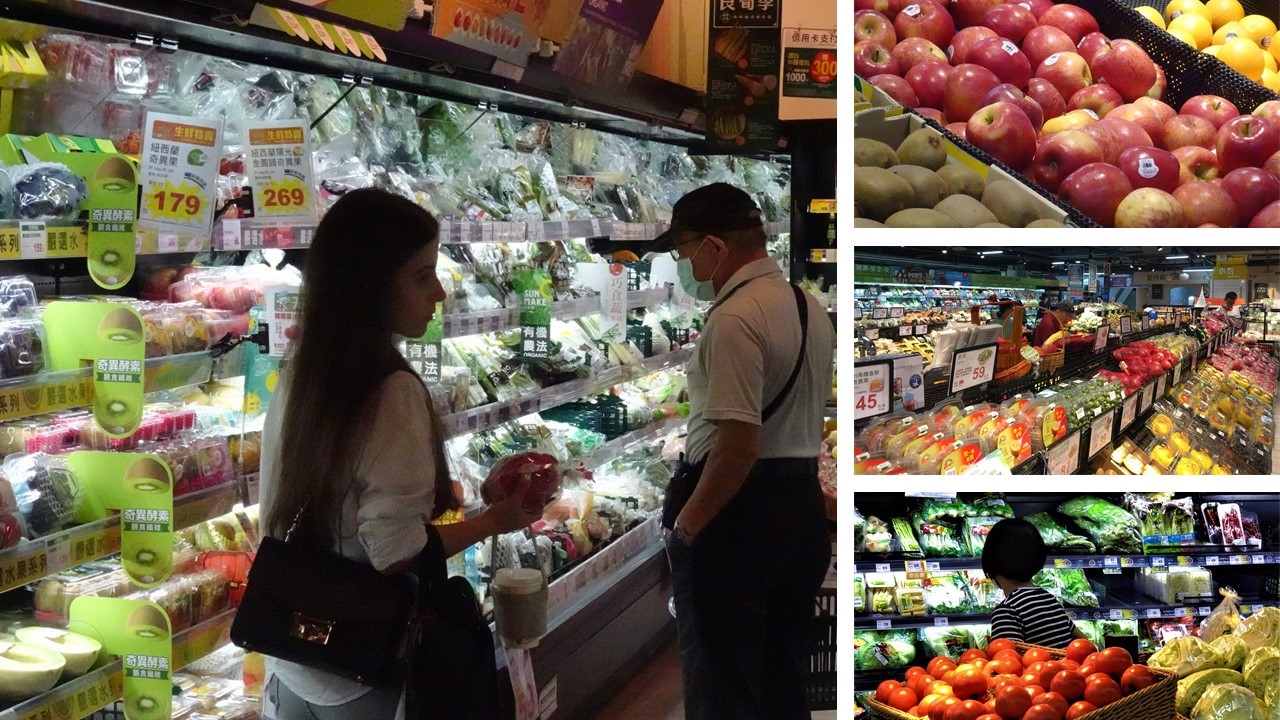

Dynamic and constantly evolving

By Mike Jewell

The announcement that Carrefour is to buy all of Dairy Farm’s Wellcome and Jasons Market Place stores and associated distribution facilities in Taiwan, subject to regulatory approval, is set to bring about a major change to the landscape of food and grocery retailing.

This is the latest step in the continuing transformation of this sector over the past three decades from a traditional format centred on wet markets and “mom-and-pop” stores into a very modern shopping environment, integrating the latest in bright, sleek in-store design and customer offers with cutting edge e-commerce.

Behind this change is one factor that marks Taiwan out as different from many developed markets around the world – the need for retailers to have a substantial presence on the ground, in terms of store numbers, in response to consumers’ desire to shop “nearby”. As Guillaume de Braquilanges, CFO at Carrefour Taiwan commented: “Taiwan is a market of convenience.”

Many companies have fallen by the wayside, as they failed to achieve the critical mass needed for a sustainable business. While there has been an explosion in the number of food and grocery outlets, we have also seen considerable consolidation within the industry, with smaller chains and independents being absorbed by larger competitors. Carrefour’s swoop for the Wellcome/Jasons network is the most spectacular example of this.

Since 1990, the number of so-called modern trade outlets has grown over five times to almost 14,000. In the early 1990’s, in addition to the ubiquitous wet markets and independent mom-and-pops, there were:

- 2,300 convenience stores (CVS), of which 800 were 7-11, 150 Circle K (now OK Mart), 145 Family Mart and 70 HiLife;

- 15 hypermarkets, of which 7 were Makro and 6 Carrefour

- 260 supermarkets, of which 70 were Wellcome, 51 Hsin Tung Yang, 22 ParknShop and 19 May Tsung.

Today is vastly different:

- 11,400+ CVS, of which 5,400 are 7-11, over 3,300 are Family Mart, 1,300+ are HiLife and almost 900 are OK Mart;

- 117 hypermarkets, of which 67 are Carrefour, 20 are RT Mart, 14 are A Mart and 13 are Costco;

- 2,400 supermarkets, of which almost 1,000 are PX Mart, 670 are Simple Mart, 199 are Wellcome and 69 are Carrefour Market.

What is also striking is the extent to which a small number of brands now dominate – in 1993, the top four accounted for 51% of all CVS outlets, while the four leading supermarket chains had 62% of the total stores. Currently 7-11, Family Mart, HiLife and OK Mart own 96% of all CVS outlets and a combined 81% of all supermarkets belong to PX Mart, Simple Mart, Wellcome and Carrefour.

Carrefour has maintained a strong focus on expanding store numbers ever since entering the market and in recent years has concentrated on increasing the number of Carrefour Market supermarkets. At a rate of around 20 new outlets per year, this has provided steady, but slow growth. The acquisition of Wellcome/Jasons will effectively provide 11 years’ growth at a stroke.

One industry analyst noted in a recent article in Commonwealth Magazine:

“In the second half of last year, Carrefour noticeably slowed down its expansion of Carrefour Market proximity stores, I guess it has decided to expand through acquisition. Snatching up good locations with one deal is much better than painstakingly expanding one location at a time.”

De Braquilanges summarised the impact of Carrefour’s expansion this way:

“It’s a big change in terms of visibility, the number of points of contact with the customers will increase significantly, with the opportunity for us to provide a wider set of services to the customers.”

Kantar Worldpanel estimates that Carrefour will instantly gain access to an additional 400,000 households and 10 million shopping trips annually, lifting its supermarket business by over 350% and its total revenues will now overtake Costco’s.

Furthermore, the concentration of Wellcome’s locations in Taipei and northern Taiwan will significantly strengthen Carrefour in this key area of the island.

The growing importance of local supermarkets

Even with the modernisation of the grocery trade, Taiwanese shoppers still maintain a fairly traditional approach to buying food and grocery, shopping frequently across a wide repertoire of stores. According to Kantar Worldpanel, the average consumer shops in more than ten different channels each year.

The main factor governing the choice of outlet is the nature of the shopping trip – is it a big trip to stock up on a wide selection of household necessities or is it to buy a small number of items for today or tomorrow’s meals? Or perhaps the shopper just needs something now, something which has suddenly run out or which they want to take back to the office.

Carrefour recognises that shoppers’ “missions” do vary and aims to capture as wide a range as it can with its integrated portfolio of both hypermarkets and supermarkets. Carrefour is unique in Taiwan, being the only grocery retailer operating more than one type of bricks-and-mortar outlet.

Guillaume de Braquilanges explained Carrefour’s philosophy this way.

“What we want to create is a kind of ecosystem, with different missions and different destinations, too. [With hypermarkets] there is something very important. We are operating the hypermarkets most of the time with shopping malls, which makes a big difference, because it is an additional reason to go and shop there. It’s not just about shopping for groceries, but it’s an experience to go to the boutiques and the food court and so on. We are operating this format really as a combo.

And these hypermarkets have a really clear mission, as a destination for the big purchase, with the biggest assortment you can have, with competitive prices, with choice, with innovation, with services also, with activities. It’s partly entertainment. This is the experience we want to provide and there’s definitely a market for that.

The supermarkets are different. Their mission is really being close to home, giving the customer the opportunity to have a good assortment to shop on a daily basis. That means you will get competitive prices, but of course a more limited range of products, but still enough for you to do your daily shopping. And the advantage [for us] is having a lot of contact points around local neighbourhoods.

Hypers in shopping malls and local supermarkets are really complementary, giving us an efficient commercial offer.”

Statistics from the Ministry of Economic Affairs show that supermarket sales are still slightly lower than hypermarket sales (NT$207 billion vs. NT$210 billion), but are growing at a much faster rate, along with the rapid jump in store numbers. From 2012-19, supermarket revenues rose by 44%, compared with a 24% increase for hypermarket sales. The consensus across the industry is that supermarkets are fulfilling an increasingly important role, tapping into consumers’ desire for proximity and convenience, as well as aligning with the long-term reduction in household size in Taiwan.

Peggy Liu, Senior Business Development Manager at Kantar Worldpanel, explained:

"They [Carrefour] are following the market trend in developing supermarkets, because in Taiwan, household size keeps shrinking. Now per household it's only around 3 people, which means we don't really need to stock up from hypermarkets that much. For daily use or more frequent things, weekly grocery shopping, I'll go to a supermarket. That's the trend now."

Figures from market researcher Nielsen also underline this shift. In the year to May, sales of fast-moving consumer goods (FMCG) grew by 5.6%, but hypermarkets saw sales increase by just 1.9% (despite a strong performance by Costco), as against 10.1% growth in PX Mart and 5.7% growth in other supermarkets.

Food is the key category, making up about 65% of FMCG sales and, as a daily necessity, is the main driver of regular store visits. Kantar Worldpanel estimates that hypermarkets and supermarkets account for similar proportions of food sales (excluding fresh produce, which they are unable to measure), at 27.1% and 29.0% respectively. Again, Nielsen has seen a stronger performance in PX Mart (+12.5%)  and other supermarkets (+5.8%) compared to hypermarkets (+3.2%).

and other supermarkets (+5.8%) compared to hypermarkets (+3.2%).

PX Mart is the leading supermarket brand, following a sustained programme of expanding its footprint and revitalising its offer. After its transformation in 1998 from the post exchange format, open only to military personnel and government employees, PX Mart built up its store numbers through new openings and acquisitions to its current level of around 1,000 and sales of NT$100 billion. Kantar estimates that PX Mart now counts 90% of Taiwan’s households as customers.

Initially, the company followed the traditional model of just selling dry and packaged groceries from what were often rather uninviting premises, but at least the prices were low to keep Taiwan’s price sensitive consumers coming back, especially as the stores were easy to get to. At that time, fresh meat, fish, fruit and vegetables were bought from traditional wet markets, with consumers’ unshakeable faith in the quality and freshness of their products.

However, the PX Mart strategy changed in 2008, when senior management began introducing new ideas from abroad, particularly Japan. According to Commonwealth magazine, Chairman Lin Min-hsiung was particularly struck by a comment from the honorary chairman of the Japanese Supermarket Association:

“Dry goods are susceptible to cut-throat price competition; supermarkets that fail to incorporate fresh produce are bound to be eliminated from the market.”

Fresh products began to appear on PX Mart shelves and now account for 20% of revenue and most other retailers, notably Carrefour, are focusing just as intensively on the fresh category.

“Fresh is key” says de Braquilanges, explaining that the range and quality of goods on offer is a trigger for choice of outlet and builds loyalty among customers. It ties in very much with the ever increasing interest in health and wellness in Taiwan generally and Carrefour’s offer is expanding all the time in both hypermarkets and supermarkets, beyond regular produce to encompass more specialised items such as organically produced food, gluten-free items, sugar-free products and so on.

Shoppers are increasingly seeking reassurance as to the quality and safety of the foods they are buying, especially following the shock of several food scandals, when consumers had previously felt Taiwan was immune to such malpractice.

Carrefour and other retailers are taking the initiative to build trust and confidence among their target audience with, for example, support materials that illustrate the journey from the farm to the customer. And Carrefour has committed to eliminate all battery-farmed eggs from its stores by 2025 under its “Act for Food” initiative, while PX Mart is incentivising farmers to stop using harmful pesticides in their production of fruit and vegetables.

Such initiatives are clearly having a positive impact on business for the modern trade, particularly this year, when the coronavirus crisis has sensitised shoppers much more to the risks to health security when mixing with crowds and buying foods in traditional markets.

Nevertheless, wet markets retain much of their reputation for freshness and have a unique place in the fabric of the community as a place for social exchange between traders and customers. Though the overall business may be gradually declining, nobody expects the markets to disappear.

Peggy Liu, from Kantar, put it this way:

“Traditional markets have the 'fresh' image. Housewives will go to the market early in the morning, then come home and prepare the meals for the day. It's their routine. They believe the food from the wet market will be fresh and also the relationship they build with the shops and stands in the market has a social benefit. It's the habit to start the day with a conversation there."

A notable exception to the fresh trend is Simple Mart, the second largest supermarket chain. While steadily building its network to over 600 outlets, it has maintained a format that largely replicates the mom-and-pop model, selling only packaged products within a smaller shop area, offering no frills value for money and choosing locations close to wet markets, so that customers can easily complete their daily shopping for both fresh and non-fresh items.

Meanwhile, PX Mart, Carrefour and others are continuing to innovate. With its reach of 90% of households, PX Mart’s emphasis is moving away from simply growing coverage and onto increasing loyalty and frequency of shopper visits. The company is seeking to do this in a variety of ways, through engaging with customers more intensively via direct mail and by introducing sticker collection campaigns where the redeemable merchandise is, for example, high end international brand kitchen and tableware.

It is also responding to the modern lifestyle, where time is a luxury and convenience is a necessity, particularly when it comes to meal preparation, by offering a wide selection of ready-to-cook meals and assorted prepared sauces.

Carrefour is similarly active in reaching out to its customer base and has grown penetration across a broad cross section of the population, both younger and older. Many commentators have pointed out that Carrefour has been more successful than most other foreign retailers in tailoring its offering and product selection to the particular tastes of Taiwanese consumers, coupled with competitive pricing and a solid brand image.

While Carrefour is continuing to innovate its hypermarket offer, it is the supermarket channel where much attention will now be directed, following the addition of the 224 Wellcome and Jasons stores to its existing network of 69 Carrefour Markets. Already with an established reputation among shoppers, its greatly expanded presence will likely pose a major threat to PX Mart’s dominance of this increasingly important sector of the market.

The company has announced that all the Wellcome outlets will be rebranded as Carrefour Market, to leverage the established Carrefour reputation. However, it is also committed to incorporating into the mix the strengths of the Wellcome offer, developed over 33 years in Taiwan, such as its expertise in fresh produce management.

One further weapon in Carrefour’s armoury is its private label range, which, like Costco’s Kirkland brand, has broken away from the traditional image of own label brands as cheap, but low quality. The latest Kantar Brand Footprint report identifies Carrefour private label as the second fastest growing FMCG brand in terms of consumer choice in Taiwan.

The addition of the 25 Jasons Market Place stores to Carrefour’s stable opens up a new opportunity in the premium sector. With Jasons, Wellcome Taiwan has cultivated a loyal base of high-end customers to compete directly with department stores’ own supermarkets, as well as CitySuper. The Jasons stores will instantly give Carrefour market leadership in this niche, but strategically important segment. What changes Carrefour will make to the Jasons format have yet to be confirmed, but it is clear that the company values its established premium positioning and is intent on preserving it.

One further aspect that the leading supermarkets have paid close attention to in recent years is consumers’ desire for a “pleasant shopping environment”. PX Mart has invested heavily in upgrading many of its stores and introducing ancillary services, while Carrefour Markets also offer some of the wide range of services provided by convenience stores, including seating areas.

Supermarkets are building a “local lifestyle ecosystem, offering a broader range of services to satisfy consumers’ daily needs,” according to the Market Intelligence & Consulting Institute (MIC). This is a massive step forward from the shabby, cramped and untidy stores that were common as recently as a decade ago and even the more traditional minded Simple Mart has begun experimenting with updated store formats, presumably in recognition of the trend elsewhere in the industry.

The rise and rise of e-commerce

Despite Taiwan being a highly digitised and internet-savvy society, online shopping for consumer goods was slow to take off. That has now changed dramatically, with several FMCG categories seeing double digit growth in the past 2-3 years and major retailers have embraced the growing channel enthusiastically, alongside numerous pure players.

Kantar Worldpanel estimates that online sales account for 10.4% of FMCG sales and fully 16.3% of non-food lines. Online food sales have lagged behind but are now growing strongly and reached 7.4% share in Q1 this year. The coronavirus pandemic has given e-commerce a big boost, with more and more consumers opting for the perceived safer option of buying online and it’s not just younger, tech-savvy individuals choosing this route, but a broad range of shoppers, including many older first-time buyers, resulting in as much as 30% year-on-year growth in online sales in May.

Even when the health crisis finally abates, the industry expects that e-commerce will sustain its robust performance, particularly for bulkier, hard to carry items and lines with an established online track record, such as health supplements and skin care, where shoppers can buy well known, imported brands conveniently.

All generally agree that online and bricks-and-mortar channels will co-exist happily, with e-commerce perhaps topping out in the range of 20-30% of sales, while physical stores, at least the ones that are able to engage most effectively with their customers, continue to fulfil the fundamental emotional desire for personal contact.

“People shop not just for the single store, but for the overall enjoyment of being in a community environment.”

James Daunt, CEO, Barnes & Noble

What next?

Carrefour’s purchase of Wellcome Taiwan has injected a new dynamic into food and grocery retailing, which has already been subject to huge change in recent years. The five-fold increase in modern trade outlets, coupled with the introduction of e-commerce, has transformed the industry. Absolute store numbers may be approaching their peak, but further consolidation can be expected, as the leading players seek to reinforce their positions, especially in the growing supermarket sector, which is offering so much of what Taiwanese consumers are looking for – proximity, convenience, quality fresh produce, competitive prices on the right selection of goods and a pleasant shopping experience. Independent groceries and mom-and-pop stores may be approaching the end of their shelf life, as premium supermarkets and organic stores move into developing niches at the top end and e-commerce becomes a mainstream channel fully integrated alongside physical shops and the still vibrant and much-loved wet markets.