Sustainability & CSR

Can Taiwan become APAC's offshore wind energy hub?

With a good head start in development, excellent location and growing talent pool, Taiwan has the potential to become the Asia-Pacific region’s offshore wind energy hub, but action will be needed to maintain momentum and increase competitiveness

By Jason Wang, Raoul Kubitschek and James McCatherin

With the development of offshore wind energy (OSW) taking off in the Asia-Pacific (APAC) region, Taiwan, as an earlier starter, is uniquely positioned to become an important part of APAC’s future offshore development. Taiwan has a treasure trove of experience when it comes to policy development, attracting international investment and know-how into the country and building offshore wind farms. As such, Taiwan has the potential to become a regional hub for supporting other countries in policy development, supplying services and equipment. However, with other countries rapidly catching up, Taiwan must play to its advantages now and accelerate its outreach efforts in order to build a unique leading position in Asia-Pacific.

According to the 2023 Global Wind Report released by the Global Wind Energy Council (GWEC), the worldwide cumulative installed capacity of offshore wind now stands at 64.3GW, with an additional 8.8GW added in 2022. Of this, China contributed an additional 5GW, Taiwan added 1.175GW, and Japan brought 84MW online. Currently, the cumulative installed capacity of offshore wind energy in the Asia-Pacific region stands at nearly 34GW, with China taking top spot in the region and globally. Taiwan comes in as a solid second place in the region when it comes to a mature market regime and construction activity.

As offshore wind power in the APAC region gains momentum, China, Taiwan, Japan, South Korea, Australia, Vietnam, and India have emerged as the most notable markets. At the end of last year the Philippines also started in earnest to make a pathway for offshore wind energy and is moving ahead fast in laying the groundwork.

Maturing markets in APAC

Outside of China, Taiwan, Japan, South Korea, Vietnam and Australia are currently leading offshore wind development in the region. As of February 2023, Taiwan has grid-connected capacity of nearly 897MW, significantly higher than Japan's 135MW. Japan is also currently running its second auction, which is adding significantly to their development pipeline and will conclude in mid-2023. South Korea and Australia do not have any operational commercial scale offshore wind farms yet. However, both governments have set ambitious targets for offshore development, which are well underway.

Australia has sparked global interest after the government announced the Offshore Electricity Infrastructure Act in late 2021 and Victoria State started to announce selected areas. Currently an auction is in full swing and will conclude in April 2023.

Vietnam, with a strong experience in intertidal (nearshore) wind farms, has also seen great interest from the international offshore wind energy community over the last three years, attracting major players into the market who have begun development of offshore wind projects in the country.

Overall, these countries are actively promoting their own offshore wind industries and developing the necessary infrastructure, creating employment opportunities, and driving technological progress needed to become major players.

Newcomers

Over the last two years we have also seen the advent of other countries in APAC, such as the Philippines, Bangladesh, India, Indonesia and New Zealand which are now actively pursuing offshore wind power development.

In the Philippines, the World Bank released a comprehensive roadmap to offshore wind development in 2022, followed by feasibility studies financed by other development aid agencies, such as USAID and the Asian Development Bank (ADB). At the end of 2022 the Philippines' Department of Energy approved at least 42 offshore wind service contracts with a total capacity of 31.5GW, surpassing the World Bank's expected potential. Just last week, the government issued a decree to speed up the development of a one-stop permitting system in the Philippines.

In India, the government is investigating the potential of 35GW and 36GW of offshore wind, respectively, off the Tamil Nadu coast and Gujarat coasts. In Indonesia, according to data released by its Ministry of Energy and Mineral Resources (ESDM), the potential for offshore wind power is about 94.23GW. However not all those opportunities are likely to be commercially attractive. Bangladesh has initiated a feasibility study for offshore wind with a loan extended by the ADB.

Outside of New Zealand, development in these countries as well as Vietnam are expected to be bolstered significantly by investment and de-risking support from development banks such as the World Bank, the ADB and other international donor agencies and international development aid institutions. These organisations have their sights set on supporting developing countries in their respective energy transition in accordance with the UN’s sustainable development goals. With booming economic growth projected, the need to electrify more areas in Southeast Asia, and the shifting of supply chains beyond China, the demand for green energy in Asia is expected to increase significantly. Offshore wind power will be a key area of development in the foreseeable future.

The successful experience of Taiwan

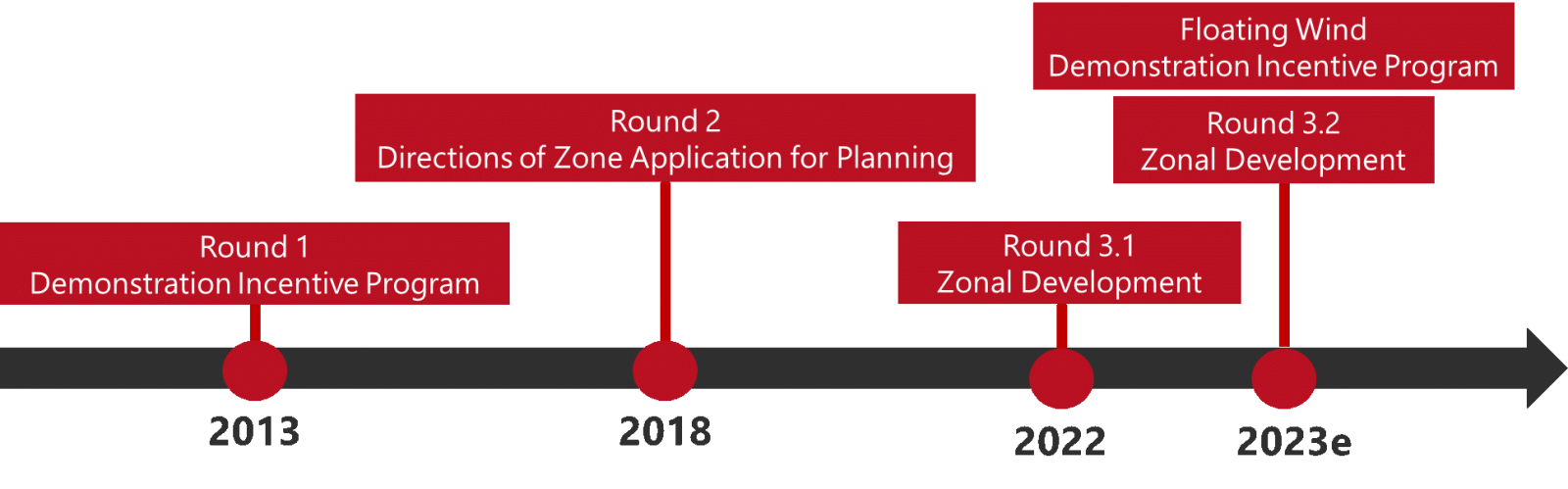

Taiwan is uniquely positioned to play a pro-active role in the region. Offshore wind development in Taiwan has progressed in the last ten years through three stages of policy formulation and execution: the Round 1 Demonstration Incentive Program from 2012 to 2021 (237MW), the Round 2 Directions of Zone Application for Planning from 2016 to 2025 (5.5GW), and Round 3 Zonal Development from 2026 to 2031 (15GW). In addition, to develop offshore wind farms in deeper waters, Taiwan has also prepared a Demonstration Incentive Program for floating wind power, set to be promulgated at the end of 2023. In March of this year Taiwan connected it’s third offshore wind farm, Formosa 2, with a capacity of 327MW, to the grid. Two more wind farms are expected to be connected to the grid this year: Changfang & Xidao (Phase 1), and Greater Changhua 1 and 2a, respectively. More projects are under construction and will follow over the course of the next four years to completion.

In addition to attracting international developers through the three-stage development process, Taiwan's localisation strategy, while not yet fully implemented and subject to criticism from wind industry players, has at least managed to successfully either attract direct investment into Taiwan, and established joint-ventures or enabled domestic manufacturers to participate in different stages of development, thereby allowing Taiwanese professionals to hone their skills on related technologies to expand production capacity and create new and high-skilled jobs.

Over the course of more than a decade Taiwan has successfully tested and adopted a framework for offshore wind energy that has attracted billions of US dollars in international investments, mainly from the Europe, the pioneer in offshore wind energy, and also from Japan and the US. This has created thousands of high-skilled and well-paid jobs as well as allowed new Taiwanese companies to flourish or traditional companies to pivot into a new market.

Could Taiwan truly form an APAC hub?

Given the current progress of offshore wind development and the capabilities of companies in Taiwan, backed by both foreign and local investors, Taiwan has the potential to become a commercial hub in APAC and to expand its trade ties and engagement with governments in the region on offshore wind industry development. Due to its unique international status Taiwan is often overlooked by other countries, which means Taiwan needs to be far more proactive in promoting itself and its industry in the region. For example, Taiwan is a member in the ADB, and it would benefit to have more dialogue on that level, as well as building on the current "New Southbound” strategy.

This would have enormous economic and political benefits for Taiwan. Taiwan’s likely advantages could be as follows:

- Taiwan's policy has entered the stage of competitive bidding. Many countries in the APAC region, especially in Southeast Asia, have not yet formulated a complete offshore wind development policy or strategy. Taiwan can be seen as a successful case study in the region in promoting offshore wind which could help other countries in the region to better understand the challenges and opportunities in developing an offshore wind energy market.

- Many financial institutions in Taiwan have now invested in offshore wind projects and are gradually cultivating their capabilities to participate in the international financing market. In the future, there is an opportunity for Taiwan to diversify and participate in offshore wind power projects in the APAC region.

- Taiwan's location is ideal, being centrally located between Southeast Asia, Japan, and South Korea. Taiwan could serve as an excellent operational centre for a regional offshore wind supply chain.

- With almost seven years or more of experience, Taiwan’s green collar talent pool is considered excellent within the region, built on a strong educational system, as well as bolstered by government support and numerous industry training programmes in collaboration with international industry players to continually cultivate new talent. This talent pool can be deployed to support regional offshore wind energy projects.

However, there are also numerous obstacles and challenges to overcome, which could jeopardize Taiwan’s position as a regional leader. Although Taiwan’s financial market has started to invest in offshore wind projects in Taiwan, the level of international participation of local financial institutions remains limited, also due to regulatory challenges, and there is still a shortage of professional talent in that sector to track and manage the development and risk of offshore wind projects.

In addition, while Taiwan's local supply chain capabilities are growing, neighbouring countries such as South Korea and Japan are vigorously developing their own local supply chains and expanding their production capacities rapidly. Taiwan’s policy would also need a stronger focus on making local suppliers globally competitive as many equipment suppliers in Southeast Asia have begun to invest in resources and are competitive due to a variety of factors, including the low cost of labour.

Another challenge for Taiwan is that it is often left out of international trade agreements for political reasons, again providing barriers to Taiwan’s competitiveness and ability to participate. A home-made commercial hinderance for Taiwan to serve as an APAC headquarters is its archaic withholding tax system. If companies are to provide international services through Taiwan, they need to include other offices’ services to package them towards overseas markets. However, Taiwan’s 20% withholding tax (and/or a complicated application system to lower it) makes it cumbersome to work via Taiwan on overseas projects. Companies also do not have the option to agree with their headquarters or overseas subsidiaries on yearlong frameworks to call off services for different projects and/or clients overseas. This means that each project handled by a Taiwanese company will be treated individually, adding significantly to transaction costs and the administration burden. There is a need to reform this in order to elevate Taiwan’s attractiveness as a regional hub to countries like Japan, Australia or Singapore.

According to PwC's report "The next frontier for infrastructure investments", the Asian region is predicted to see up to US$250 billion of new investment flowing into utility scale renewable energy projects by 2025. If Taiwan wants to be a major player in this transition, it is imperative that Taiwan’s offshore wind sector begins to look outward to foster its position throughout the region. Harvesting this potential in the region needs the full support of all diplomatic and external trade tools available to Taiwan. This will require both public and private leaders in the industry to maintain an international growth mindset which cultivates cooperation, innovation, and efficiency, with the goal of establishing Taiwan’s place as a centre for offshore wind energy in the APAC region.

Jason Wang is a Senior Economist for NIRAS, a Danish multi-disciplinary engineering company, focused on energy policy and market forecast consultancy for clients and supporting NIRAS’ efforts in Environmental Social and Governance (ESG) offerings in the APAC region.

Raoul Kubitschek has worked in Taiwan’s renewable energy sector since 2008 and is currently the Taiwan Country Manager for NIRAS. He is concurrently Co-Chair of the ECCT’s Energy and Environment committee.

James McCatherin is an intern at NIRAS, working on energy policy, stakeholder mapping and engagement as well as energy market research.