Sustainability & CSR

The power and potential of floating wind energy

Floating offshore wind will be essential for Taiwan to achieve its offshore wind energy goals but getting there will require the government and industry to resolve the administrative, infrastructure and financing challenges

By Jason Wang, Fredy Huang, Raoul Kubitschek and James McCatherin

A floating wind turbine off the coast of Goto Island, Japan

Source: CC

According to the report “Net Zero by 2050: A Roadmap for the Global Energy Sector” published by the International Energy Association (IEA) in 2021, over 50% of CO2 emissions reductions will depend on emerging technologies, that are currently in prototype or early stages of their development phase. Floating offshore wind is one of them and is gaining attention and traction globally as it shows great potential by allowing the installation of wind turbines in areas of the oceans that are not suitable for fixed bottom wind turbines. A floating wind platform can be installed in areas of relatively deep water, that are usually further away from the shore and thus have higher and more consistent wind speeds. Floating wind also has the potential to achieve lower ecological impacts and once scaled-up it could offer cost decreases as there is less offshore installation work needed compared to fixed bottom structures. With technological advances, floating wind will play an essential role in increasing green energy capacity and reducing CO2 footprints.

Global outlook

The 2022 Global Wind Energy Council (GWEC) annual report predicts rapid growth in the global floating wind energy market. This market segment has potential upward projections of 180 GW of installed global capacity by 2050, comprising of nearly 13,000 floating turbine units[1]. GWEC’s global wind report highlights that although fixed-bottom offshore wind currently dominates the industry, floating has the potential to account for 80% of total offshore wind capacity in the future. A number of European countries including the UK, France, Denmark and Portugal, are actively launching demonstration and pre-commercial projects for floating wind. Countries in the Asia-Pacific region, including Taiwan, Japan, and South Korea, among others, have also incorporated floating wind power into key policy documents. Since the Fukushima incident in 2011, Japan has invested in demonstration projects to test different floating wind technologies out at sea. South Korea has specifically included floating wind in its energy goals with more than 6GW already in the pipeline. Taiwan also has a history of looking into floating wind with two projects having been proposed for Round 1 of wind power development plans going back as far as 2016-17 as well as basic research by local think tanks going back to the 2010s. However, for various reasons, both proposed projects went no further than the Environmental impact Assessment process.

Taiwan outlook

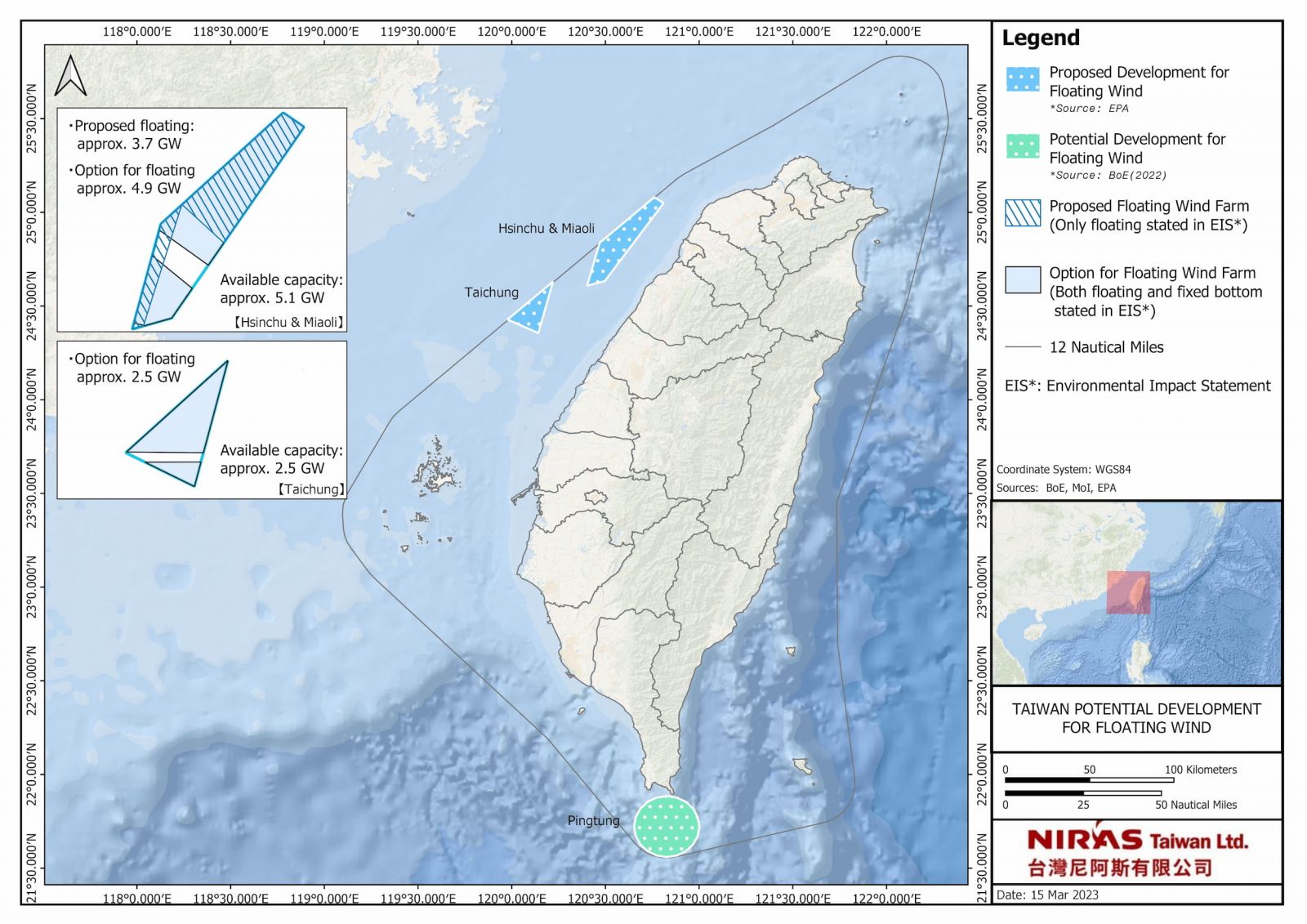

In recent years, Taiwan has primarily focused on developing fixed-bottom offshore wind infrastructure, resulting in a cumulative installed capacity of 745MW by the end of 2022. Taiwan has already granted grid allocations to achieve 5.6GW by 2025 and plans to install 1.5GW annually from 2026 onwards, with the aim of reaching 13.1GW by 2030 as part of Round 3. Originally, the Bureau of Energy (BOE) had anticipated that floating wind would be fully commercially competitive by 2031 without any supporting mechanism and able to compete against fixed bottom. Developers have been actively preparing and considering floating wind projects, an approach in line with Taiwan's ambitious 2050 net-zero emissions roadmap, which has an offshore wind capacity target of 40-55GW by 2050. If already the current projects are successful – and discarding overlapping developments, there is already sufficient area proposed to allow approximately 7.6GW of potential floating wind capacity to be installed. This would eclipse the currently awarded 5.6GW of capacity for fixed bottom capacity by 2025 and would strongly support the 15GW goal of additional new capacity between 2026 and 2035. Going forward, allowing developments outside of the 12 nautical mile zone, as supported by the new Renewable Energy Development Act, and revisiting some excluded areas, the potential for floating wind would be likely sufficient to help reach 2050 goals. In light of these activities and considering overseas experience with floating wind, the BOE last year considered offering a separate floating wind development track to pull forward the original timeline and to allow Taiwan to speed up the deployment of floating wind. This also means that there is the opportunity for Taiwan to regain its leading position in the region when it comes to the offering a potentially robust investment framework and a timeline backed by political will.

Currently proposed floating wind energy sites and potential in Taiwan based on public information of the Environmental Protection Agency and BOE (as of 15 March 2023)

Acknowledging the fact that floating wind needs a different development road to market compared to fixed bottom projects and is not yet commercially competitive compared to those projects, the BOE last year proposed a demonstration project framework for floating wind. The BOE aims to assess the feasibility of floating wind in Taiwan and provide policy support to build up to three projects with a Feed-in-Tariff mechanism. Those projects should help to further understand the need for and demands of infrastructure, installation techniques, joint research and development, regulatory changes as well as the environment and social impacts of floating wind. It will also provide important lessons for the market to pave the way for competitive auctions for large scale projects at some point.

In January 2023, BOE held a second public briefing regarding demonstration project with following key take aways:

1. The deadline for grid connection was extended from 2026 to 2028.

2. Projects need to have obtained at least a conditionally-approved Environment Impact Assessment. (At time of writing only one project has managed to do so and a second is close to completion. Other projects are still pending a first panel hearing.)

3. The capacity cap of a single floating wind farm has been adjusted from the original 50MW to 6-12 floating platforms without a fixed capacity limit. Assuming the deployment of 15MW wind turbine generators, each project’s capacity could reach 180MW.

4. An additional project can be awarded alongside the two that were originally proposed.

5. Academic-industrial cooperation has been added into selection criteria instead of mandatory localisation requirements.

6. The bidding deadline is expected to be towards the end of 2023. However there has been no written statement on a concrete date so far.

The increase in capacity of the demonstration project has received positive feedback from industry players, although they had originally proposed a size of up to 200-250MW per project on the grounds that larger projects would benefit from economies of scale and more closely mirror future real projects in terms pre-commercial testing, installation and logistics.

Taiwan's active promotion of floating wind demonstration projects and the inclusion of floating wind turbines in its medium to long-term development energy goals is due in part to several factors which inhibit growth of fixed bottom technology. Although Taiwan is surrounded by the sea, offshore wind energy is only one of the many maritime users and the government must consider issues such as national defence, navigation safety, aviation safety, fishing, and the development of marine tourism. Therefore, because of these limitations, Taiwan is running out of suitable areas for fixed bottom development for the next phase of development (Round 3.3, scheduled for 2024). Since floating wind can be used to develop wind farms in more distant and deeper waters, they are the only option to achieve Taiwan’s goal of 20.6GW of accumulated offshore wind energy capacity by 2035. If Taiwan is to achieve 40-55GW by 2050, a holistic approach to marine spatial planning is necessary while there is already a need for a centralised coordination of all agencies and major stakeholders involved in maritime usage and/or protection. Originally there were also floating wind areas proposed by private developers in the north of Taiwan but those were not able to be used as other maritime users got precedence for these areas.

Creating a robust framework for floating wind in Taiwan

Despite its significant potential, floating wind development needs to overcome hurdles to succeed.

Infrastructure, especially ports, is an obvious constraint. Taiwan does not have the luxury to make one or two ports mainly available for the offshore wind industry as there is a strong existing demand from multiple users on port facilities. Taiwan's suitable ports are already working at or above capacity just to meet the needs of fixed-bottom wind projects, creating bottlenecks and frequent project delays. The port authorities, while highly supportive of this new industry, are constrained in their options for a quick expansion of facilities. On top of the already existing challenges, floating wind construction requires larger ports and wet storage areas to optimise installation procedures.

In addition to infrastructure, floating wind developers can face challenges in securing financing and related funding from banks and investors as Taiwan is still a test bed for this emerging technology. Not only are there challenges on the technical side, but they also include policy issues such as a lack of a fully formulated regulatory framework. The said frameworks, which among others, include standardised methodology and criteria in assessing the impact on the fishing industry, the capability of withstanding typhoons, or operations and maintenance (O&M) challenges, are essential to the industry’s efficiency, reputation, and ultimate success of Taiwan’s renewable energy goals. To overcome financing challenges the government’s approach is currently to offer a yet to be decided Feed-in-Tariff, which will be key to securing the viability of projects. Similar positive effects would apply if government-owned banks are supportive of guaranteeing or making special loan vehicles available for companies that want to invest into building capacity for floating wind and/or developers to invest in projects.

To facilitate the development of floating wind in Taiwan following policy tools could elevate Taiwan’s ambitions:

1. Given the financial challenges faced by some offshore wind projects in Round 2 and the higher costs associated with floating wind compared to fixed-bottom, financial support and incentives need to be provided to encourage the development of floating wind projects.

2. Considering preparations of last year’s Round 3.1 fixed bottom auction, the government's policy planning and administrative procedures would benefit from a streamlined and transparent approach. For example, a complete administrative contract, infrastructure planning, a wind farm overlap conflict resolution mechanism, a known Feed-in-Tariff and other supporting measures should be disclosed to the public and developers six months before the bidding deadline for the demonstration projects. A six-month window with a full set of information would allow project owners to engage with international and local supply chain operators as well as government and public stakeholders and allow for a sound investment plan to secure the viability of these projects.

3. Taiwan’s port authority is in a Catch-22 situation. There is not yet a clear installation target for floating offshore wind, making it difficult to plan for the needed long-term infrastructure investments. The government has also not yet released a medium- to long-term port construction plan that takes floating wind development into consideration. The port infrastructure needs of floating wind turbines differ greatly from those of fixed wind turbines, and the lack of port planning could seriously affect the engineering and grid connection schedule. In addition to the demonstration project, there should also be a long-term installation goal for floating wind, similar to what has been set for fixed bottom. This would allow harbour authorities to plan for temporary or permanent quayside and hinterland investments.

4. Floating wind still requires a large number of new and innovative technologies. Given the current state of Taiwan's domestic supply chain for offshore wind, which still needs breakthroughs in production capacity and technology, it is necessary to propose technical research and development or testing subsidies specifically for floating wind. Furthermore, research and development and academic resources, international industry-academia cooperation, and cross-border government cooperation should be linked to accelerate the technological development of floating wind in Taiwan.

To ensure the long-term growth of offshore wind, the government can capitalize on developing and maturing floating wind in Taiwan. This requires a re-examination and evaluation of regulations, administrative procedures, infrastructure, talent development, financial mechanisms, optimisation of local supply chain capabilities, and technological innovation for floating wind. Learning from the lessons of Round 1 & 2 as well as Round 3.1 it is essential to establish a solid foundation to support their growth and success.

For Taiwan, floating wind is key to achieving its renewable energy goals as it will allow tapping into areas that are unavailable to fixed bottom projects. This would further reduce Taiwan's reliance on imported energy and lower its carbon emissions. In addition, the continuous introduction and development of innovative technologies can help Taiwan to use green growth as a foundation for future economic development. Given Taiwan’s strength in engineering and manufacturing, there is strong potential to develop a thriving floating wind energy industry in Taiwan in collaboration with international partners that is comparable to the semiconductor industry.

Jason Wang is a Senior Economist for NIRAS, a Danish multi-disciplinary engineering company, focused on energy policy and market forecast consultancy for clients and supporting NIRAS’ efforts in Environmental Social and Governance (ESG) offerings in the APAC region.

Freddy Huang is a licensed Professional Civil Engineer in Taiwan and is currently a Technical Consultant for NIRAS, focused on construction, fabrication, and infrastructure issues, such as port strategy planning and floater type evaluation.

Raoul Kubitschek has worked in Taiwan’s renewable energy sector since 2008 and is currently the Taiwan Country Manager for NIRAS. He is concurrently Co-Chair of the ECCT’s Energy and Environment committee.

James McCatherin is an intern at NIRAS, working on energy policy, stakeholder mapping and engagement as well as energy market research.